Bonus depreciation has expired -- now what? For the last two years, thousands of companies took full advantage of the stimulus provisions found in the Economic Stimulus Act of 2008. In particular, the bonus depreciation provision allowed businesses to claim 50 percent of an asset's tax basis as "bonus depreciation" and still claim the regular depreciation on the remaining basis. By taking bonus depreciation, many of these companies paid little to no tax during these two years.

But since bonus depreciation expired at the end of 2009, the question remains -- now what? Is it possible for businesses to reap the same type of tax benefits without bonus depreciation? Yes. Under section 1031 of the Internal Revenue Code, these companies can structure the sales and purchases of their business assets as like-kind exchanges and continue to recognize substantially less tax gain.

A company that routinely buys and sells business assets can implement an ongoing, repetitive like-kind exchange program (commonly referred to as an "LKE Program"). For example, an equipment dealer with a fleet of rental equipment can implement an LKE Program and defer the tax that would otherwise be owed upon selling the equipment. A sale of old rental equipment and purchase of new rental equipment can be treated as an "exchange" for tax purposes. The IRS even released a Revenue Procedure in 2003 that provides certain safe harbors to companies that implement LKE Programs.

The following example demonstrates the benefits of bonus depreciation and LKE Programs. To more easily highlight the reduced tax and increase to cash flow, this example assumes that ABC Co. buys $10 million of rental assets every year, and sells those assets two years later for $8 million. The facts are as follows:

- Annual Acquisitions of Rental Assets = $10 million

- Annual Dispositions of Rental Assets = $8 million

- Average Hold Period = 2 years

- Average Residual Value = 80%

- 5-Year MACRS / DDB Method / Half-Year Convention

- Combined Tax Rate = 40%

- Fleet Growth = 0%

- Inflation = 0%

- Annual Rental Income = $10 million

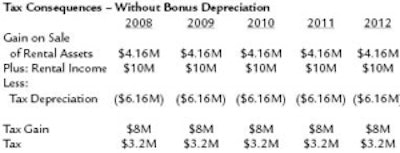

Based on these facts, the tax consequences to ABC Co. without bonus depreciation are shown in "Tax Consequences - Without Bonus Depreciation".

The ability to take bonus depreciation on the rental assets acquired and placed in service during 2008 and 2009 has the impact on the tax consequences as shown in "Tax Consequences - With Bonus Depreciation".

When comparing the tax consequences between the two scenarios, the first thing to notice is the positive impact on cash flow that bonus depreciation had in 2008 and 2009 before it expired. Over the course of those two years, bonus depreciation allowed ABC Co. to increase its depreciation expense by $6,400,000, and reduce its total tax liability by $2,560,000.

However, the amount of tax paid by ABC Co. skyrockets from 2009 to 2010 as a result of two things. First, the bonus depreciation assets acquired in 2008 are being sold in 2010. The low tax basis in these "bonus assets" results in more gain from the sale of rental assets. Second, there is less tax depreciation taken in 2010 since the bonus depreciation was taken upfront in 2008 and 2009. As a result, the entire benefit of the bonus depreciation is given back to the government during 2010 and 2011.

By implementing an LKE Program in 2010, ABC Co. is able to solve the tax problem created by the expiration of bonus depreciation. The company no longer has to give back the benefit of the bonus depreciation. As illustrated in "Tax Consequences - With Bonus Depreciation & 2010 LKE Implementation", the benefit is essentially extended by implementing the LKE Program.

Is it a known fact that Congress will not extend bonus depreciation through 2010? No. Trying to predict what the government is going to do is more difficult than trying to predict the stock market. But the provision for bonus depreciation was not extended in The Worker, Homeownership, and Business Assistance Act. It also was not extended in the Hiring Incentives to Restore Employment (HIRE) Act back in March of this year, or in any other legislation. Although it might not feel like it, the government has been indicating that the economic recovery is underway and that further stimulus is not needed.

The best thing about an LKE Program is that it is not dependent on the whims of legislators. A like-kind exchange is commonly referred to as the ultimate stimulus provision. There's no need to write letters to Congress every year urging them to extend section 1031. It's simply a part of the tax code and has been for almost 90 years.

The benefit of the 2008 and 2009 bonus depreciation does not have to stop if the government fails to extend it for another year. An LKE Program implemented by an experienced and knowledgeable tax professional allows companies to continue to enjoy the increased cash flow.

Ronald L. Hodgeman, Esq. is a Tax Director for WTP Exchange LLC, an affiliate company of WTP Advisors. Over the last 14 years, Ron has provided tax consulting and LKE Program implementation services to numerous companies, including banks, rental car companies, leasing companies, and heavy equipment dealers. If you have any questions for Ron, he can be reached via phone (513-600-3532) or email ([email protected]).