We asked leaders in several trade associations to once again look into their crystal ball to see what’s coming in 2013. Among special interest to readers are projections for highway, residential and nonresidential construction projects, as well as employment opportunities in these markets, the cost of raw materials, and the overall economic outlook both short and long term.

Despite the relatively high level of uncertainty thanks to the recent recession, a presidential election, the fiscal cliff, and turmoil overseas, prognosticators agreed on many of the fundamental drivers in the construction industry.

Highway construction

Rental: Traveling around the country this year, there appeared to be a fair amount of highway and bridge construction. Is this perception reality or indeed were many projects left unfunded? The bigger question for our readers is what’s in store for highway construction in 2013?

Ed Sullivan, chief economist, Portland Cement Association (PCA) -- Some of what you saw was real and some not so real, depending on where you were in the country. Each state spent its stimulus money in a different way. In fact, there is still some unspent money for larger projects that require more design time.

For 2013, a new highway bill provides a two-year commitment of funding equal to the previous bill, and it takes away some uncertainty. But it doesn’t factor in inflation. When coupled with the lack of stimulus, we expect a modest decline in highway and bridge construction. There should be an uptick in 2014 and 2015, thanks in part to a pent up demand for repairs and new construction projects.

Dr. Alison Premo Black, senior economist, American Road & Transportation Builders Association (ARTBA) -- The highway and bridge construction market is mixed across the country. Contract awards for highway and bridge work are down in 28 states as of October 2012. This is a leading indicator that the value of work done in those areas will likely be down in 2013. However, contract awards are up in 19 states and D.C., showing market growth. The market is up or down within 5 percent in the remaining three states, pointing to a stable market.

Nationwide we expect the real value of pavement work in 2012 to fall by about $1 billion to $46 billion, compared to 2011. The good news is in the bridge market -- the real value of work is expected to reach a record high $29 billion in 2012.

Jeannine Cataldi, senior economist, and Karen Blanford, research manager for IHS Global Insight (IHS) -- U.S. highway and bridge construction for the first six months of 2012 was up 1.4 percent over 2011 levels for the same period of time. However, 2012 highway and bridge construction was about 3 percent below 2009 and 2010 levels for the first six months. National figures can mask the wide variability that can be observed from region to region. By the end of 2012 we expect the District of Columbia to realize a 40-percent jump in highway and street construction spending, while West Virginia will see highway and street construction decline 26 percent.

For 2013, the IHS forecast calls for spending on highways and streets to fall 5.4 percent in real dollar terms. This decline is the result of uncertainty across all levels of government. This segment will also be hampered as federal stimulus monies wane and state and local governments scale back their budgets to deal with reduced revenues. The Surface Transportation Act signed by President Obama in July essentially leaves funding at current levels, having little impact on our forecast. In the longer term, spending in the highways and streets segment should increase as aging roadways and bridges are upgraded or replaced.

Anirban Basu, chief economist for the Associated Builders and Contractors (ABC) -- Your perception was reality. 2012 saw much road construction, primarily, however, at the local level where resurfacing and other projects had been deferred for several years. Despite passage of the highway bill, uncertainty still plagued the planning necessary for larger highway construction projects.

For 2013, expect more of the same. The highway bill, which has funding available for 27 months, will defray some of the uncertainty, but larger highway and bridge projects require more time for planning. A 60-month bill would have been much preferred. Regarding the future funding of highway projects, as vehicles use more alternative energy and less gasoline, dollars generated by the gas tax will have to be supplemented by other means.

Ken Simonson, chief economist, Associated General Contractors of America (AGC) -- According to Census Bureau data released on October 1, 2012, highway construction spending in the first eight months of 2012 was 4.5 percent higher than in January-August, 2011. However, the Federal Highway Administration reported on Oct. 23, 2012 that its National Highway Construction Cost Index -- a weighted average of all bids on state highway projects -- rose 7.3 percent from the second quarter of 2011 to the second quarter of 2012. In other words, bid prices rose faster than total spending, implying that there were fewer projects this year. Going forward, it appears that funding from all levels of government -- federal, state and local -- will be close to 2012 levels, meaning even fewer projects than before if bid prices continue to recover.

Building construction

Rental: The housing market continues to sputter along. From your perspective, what level of growth do you see in new construction for both the residential and nonresidential markets in 2013? Assuming that a tight credit market is partially responsible for the slowdown, do you see credit easing in 2013?

David Crowe, chief economist, economics and housing policy, National Association of Home Builders (NAHB) -- Total housing production will increase by 20 percent in 2013 over 2012 levels. The total production will be around 900,000 units, comprised of 665,000 single-family homes and 240,000 multi-family apartments. Credit remains and will continue to remain a hindrance to a full housing recovery.

Credit is tight for both builders and buyers. Builders borrow from small community banks. Many of these institutions remain under tight regulatory control by federal banking regulators who have refused to allow prudent lending in housing markets that are seeing recovery. As a result, the inventory of unsold new homes is at its lowest level in almost 50 years. Home buyers also face unusually tight lending restrictions that have left many waiting. Qualifying credit scores are higher than they were before the boom and down payment requirements have reduced the share of first-time home buyers able to get into the market.

IHS -- Residential construction spending is forecast to increase 6.6 percent in real dollar terms in 2013. This sector is beginning to see the release of pent-up demand due to underlying demographic factors (population increases, several years of reduced household formation, and lackluster construction activity). Nonresidential construction spending is forecast to decline 2.1 percent in real terms in 2013. This market is hampered by all the political uncertainty that has led to a reduction is spending and risk taking by firms. This market will follow on the heels of the residential market, with growth coming in 2014.

We do not see credit easing significantly in the near term. If there can be a resolution to the federal fiscal situation, there may be some easing later in 2013. We do not expect this to play a role until 2014. A significant pickup in hiring, though, will increase the ranks of the employed who will be able to meet the tight borrowing restrictions.

AGC -- Multi-family housing has been the brightest star in the construction firmament in recent months. Single-family construction has also risen sharply of late. For 2013, the rental market -- overwhelmingly apartment construction -- should continue to perform very well. But single-family construction could stall at a relatively low level.

Private nonresidential construction should do slightly better in 2013, led by power and energy projects, manufacturing construction, private colleges and universities, and hotels. But the big retail and office markets will languish. Public construction is likely to drift slightly lower, just as it has in 2011 and 2012.

PCA -- The housing market has been plagued by high inventories and low prices. Inventories, however, are coming down and prices are beginning to rise. Foreclosure activity has slowed somewhat, which has a positive impact on prices. Look for a 20-percent increase in residential construction, which also includes a brighter outlook for multi-family homes.

ABC -- 2013 should be a decent year in construction growth, with residential housing setting the pace. Many non-residential projects, however, will likely remain on hold due to uncertainties over the election, the fiscal cliff, Middle East strife, and the struggling economies in Spain and other parts of Europe.

The reason? There’s a more significant risk when building a hotel, office building, or shopping center than when constructing a single-family home; hence it requires more confidence in the future to go ahead with projects.

Unemployment concerns

Rental: Construction unemployment continues to outpace the national average. Do you see construction unemployment closing this gap in 2013? If so, where do you see the biggest gains, in the public or private sector, and why?

NAHB -- Construction employment should begin to pick up as residential construction gains ground. NAHB estimates that 1.5 construction jobs are added for every new single-family home built. Single-family production will increase in 2013 by 140,000 over the expected 2012 final total. At that level, there will be the need for at least 210,000 additional construction jobs.

But, construction jobs are not the only employment gains when housing production increases. The jobs to manufacture cabinets, appliances, carpets and all of the other building material components in a home are also generated with housing construction, but their counts show up in the manufacturing columns of government statistics. There will be another 210,000 ‘other’ jobs that help support housing construction for a total addition of over 400,000 jobs just from the increase in production from 2012 to 2013.

IHS -- Any closing of the gap will be minimal in 2013 as we now expect that the automatic spending cuts and automatic tax increases will be “punted down the road,” by pushing them out past the current January 1, 2013 deadline. As such, while the country will not go over the fiscal cliff at the start of January, the uncertainty that the prospect has been creating will loom further into 2013 until the issue is resolved once and for all. There will be a more significant closing of the construction unemployment gap in 2014 as the economy gathers steam. The gains will be larger in the private sector than in the public – as public funding is uncertain at best in the coming year. As residential construction gets back on its feet, this will be where construction employment lifts first.

ABC -- The construction unemployment gap should close somewhat in 2013, in part due to an uptick in residential housing construction and the fact that many construction workers have already left the industry to find work elsewhere or have retired. The bigger concern down the road will be a labor shortage for construction jobs. Potential younger workers are not learning the necessary skills to keep up with an industry that is changing – with different materials being used, different technology and different equipment.

AGC -- The unemployment rate for former construction workers has tumbled in the past two years, from 17.2 percent in September 2010 to 11.9 percent in September 2012. (Industry rates are not seasonally adjusted.) That means roughly half a million workers are no longer sitting at home waiting for a contractor to call them back. Unfortunately, construction employment has not been rising. Instead, these experienced workers have been getting jobs in trucking, oil and gas fields, manufacturing or elsewhere. It may be hard for contractors to find the skilled workers they'll need if project volumes do pick up in a year or two.

PCA -- Employment opportunities in construction will improve as building in the housing sector picks up in 2013. Nonresidential construction, especially in the public sector, will not see the same gains.

Raw materials costs

Rental: Contractors and builders often see the irony in a slowdown of projects and a rise in the cost of raw materials, may it be asphalt for road construction, steel for commercial buildings, or wood for residential housing. What are major drivers for the cost of raw materials and how do you see these costs trending for 2013?

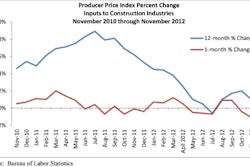

AGC -- The most problematic cost for contractors in recent years has been diesel fuel. In mid-October, the national average retail price of highway diesel hit a four-year high of $4.15 per gallon, the Energy Information Administration reported on Oct. 15, 2012. Diesel prices largely reflect global crude-oil prices but also demand for diesel from Europe and elsewhere. Anything from worries about the Middle East and a hurricane in the Gulf of Mexico to a refinery shutdown can send diesel prices soaring and leave contractors paying hefty fuel surcharges on thousands of deliveries and backhauls.

For items like concrete, gypsum and lumber, construction is pretty much the only market, and prices reflect supply and demand within the industry. Concrete prices have been flat because of limited growth of construction. Wallboard and plywood prices have spiked this year as home and apartment construction have revved up. But there is plenty of shut-in capacity that will open up if prices stay high enough.

I expect materials costs to remain volatile and to rise, on average, faster than consumer prices. But I think a 2- to 4-percent increase is more likely in 2013 than the 5-percent-plus increases that were common in 2004 through 2011.

NAHB -- Home building material costs have increased in recent months and have become more unpredictable even as housing production begins to see some small gains. The world economy has softened considerably so increased world demand is not the reason. The primary cause appears to be hesitancy in opening additional capacity on the part of building material producers. Until there is greater certainty that a housing boom is under way and here to stay, producers do not want to pour funds into re-opening plants that will not be used to their capacity. As the recovery becomes more widely spread and consistent, material price volatility should moderate.

PAC -- Lumber is still tied to residential home building. A 20-percent projected increase in that market has to be compared to how low it had dipped. Hence, the increase will likely have little impact on current depressed prices. A byproduct of oil, asphalt is impacted by the global market and its price will continue to see upward pressure from demands in China and emerging cuntries.

IHS -- More substantial price increases are on hold until the construction sector shows more sustained improvement. Prices for cement and concrete are expected to be flat in 2013 while the start of expansion in the housing sector will cause lumber prices to rise. Declining oil prices along with a bleak outlook for highway construction should serve to keep asphalt prices low in 2013.

ABC -- Until recently, raw material costs have been falling, thanks to the global slowdown. Currently, however, there seems to be a growing interest among investors to purchase commodities, creating something similar to what happened in 2008 when commodity prices skyrocketed. Not to say they will skyrocket in 2013, but raw material costs are currently misbehaving and will continue to do so in the near term.

ARTBA -- Material prices have been a big concern for the highway and bridge construction industry over the last decade. In part, this is because of volatile fuel prices, but also because getting new supply online can be a challenge. There are significant startup costs and regulations associated with opening new plants for processing cement, construction aggregates and other materials. The downturn in the overall construction industry has helped ease some of the price increases for materials since 2008, but as the construction sector comes back, it is likely that higher demand will continue to drive prices up.

Overall Economic Outlook

Rental: What do you think the impact of the presidential election will have on the overall economic outlook for 2013, in terms of the number of construction projects and overall unemployment within the construction industry?

PAC -- Politics aside, we can expect a 2-percent growth in the economy for 2013. The election, however, could make a big difference in how legislators address the fiscal cliff. Failure to come to an agreement in a timely manner will put the brakes on growth. Conversely, a timely settlement could help push growth above 2 percent to 3 or 3 ½ percent.

NAHB -- The presidential and congressional elections will not likely have a significant effect on the economy in 2013. The lame duck Congress could have a significant impact if it does not address the looming ‘fiscal cliff.' The economy remains weak with barely a 2-percent annual growth rate for 2012. Large withdrawals from the economy in the form of additional personal taxes and a reduction in federal spending will produce a recession, as will be the case if everything on the books is allowed to occur. The Congress, regardless of party control, will have to moderate these dramatic shifts but at the same time, lay a course for reduced government borrowing, which will likely mean both a reduction in federal spending and an increase in taxes.

IHS -- Regardles of the election outcome, it will take time for the smoke to clear. Will we have a government that will be able to come up with a consensus on how to resolve the debt issue? Or, instead, will we face at least two more years with each side refusing to compromise? The latter scenario would force the nation over the fiscal cliff with automatic tax increases and spending cuts being implemented. While we believe cooler heads will ultimately prevail, without a decisive victory for one side or the other, the uncertainty will preclude much construction growth in the construction industry in 2013.

ABC -- In terms of an overall economic outlook, 2013 could be a tale of two years. The first half will still be driven by a degree of uncertainty. Yet, depending on the election and makeup of Congress among other “ifs,” the second half could be better and result in a much better than 3-percent growth in the economy. There are simply too many drags on the economy to expect a growth rate greater than 3 percent.

AGC -- The White House and Congress will have a tough time avoiding massive tax increases and across-the-board spending cuts in early 2013. But the consequences of letting either take effect would be devastating for the economy in the short run. I think this will lead them to agree on some short-term extensions of current law. However, construction is almost certain to experience reduced federal funding and the expiration of certain tax credits, such as the production tax credit for wind turbines. Thus, whatever plan is agreed to, it will be costly to some elements of construction.