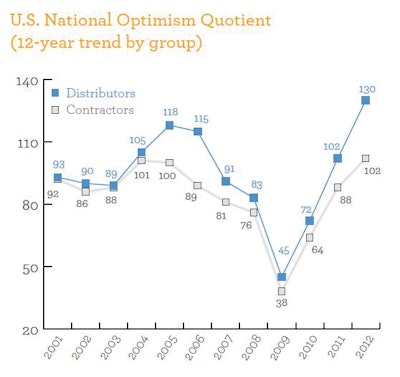

The Wells Fargo Construction Optimism Quotient for calendar year 2012 (a measure of contractor and equipment-dealer sentiment about local construction activity) is a decidedly positive 114. This is a marked improvement in optimism over the 2011 score of 96 and the 2010 score of 66. In 2009 the OQ reached an all-time low score of 42. After wading through the worst U.S. recession since the 1930s, construction executives are saying they are more optimistic that local nonresidential construction activity will improve over 2011 levels.

In general, an OQ score of 100 or more represents high optimism for increased local construction activity relative to the perceived level of activity for the prior calendar year. A score above 75 represents more cautious or measured optimism. A score below 75 signals that fewer executives say local non-residential construction activity will increase than say it will decrease -- a more pessimistic point of view.

Although 48.2% of construction executives said they anticipate an increase in local non-residential construction activity, another revealing number is that 44.0% believe non-residential activity levels will “remain the same” as 2011 levels. States with the highest expectation for a net activity “increase” in the non-residential category are Alaska, Hawaii, Idaho, Kansas and Missouri.

The sentiment for residential construction activity in 2012 is less optimistic than for non-residential activity. More than half (60.2%) of respondents said they expect similar levels of residential activity as in 2011. States with the highest expectation for a net activity “increase” in the residential category are Georgia, Montana and North Carolina.

Of the 31 executives who said they expect a decrease compared to 2011 activity levels, almost half (45.2%) said they don’t expect an improvement until Q3 of 2013 or later. States with a net “decrease” outlook for non-residential activity include New Jersey, Massachusetts, South Dakota, Virginia and Wyoming.

Of the 36 executives who said they expect decreased residential activity in 2012, about six of every ten (61.1%) said improvement would not come until Q3 of 2013 or later. States with a net “decrease” outlook for residential construction include Connecticut, Massachusetts, Oregon, Virginia and Wyoming.

In spite of a rising optimism over the last three surveys and strong optimism for 2012 that non-residential activity will improve over 2011, sentiment is still rather pessimistic about the amount of work available to sustain the current number of construction contractors. Very few executives (10.4%) anticipate an increase in the number of contractors in 2012.

About four in ten (41.7%) said they expect fewer numbers of contractors by the end of the year. However, this is an improvement over the 2011 and 2010 surveys when 53% and 73.4% of executives, respectively, said they expected fewer contractors by the end of the year.

The longstanding trend for construction equipment distributors to be more optimistic than construction contractors holds true once again. In this case, distributors are much more optimistic about construction activity levels than contractors. The 28-point difference between contractors and equipment distributors is the largest disparity in the history of this survey and dramatically exceeds the 18-point gap from the 2005 survey.

In spite of a rising optimism over the last three surveys and strong optimism for 2012 that non-residential activity will improve over 2011, sentiment is still rather pessimistic about the amount of work available to sustain the current number of construction contractors. Very few executives (10.4%) anticipate an increase in the number of contractors in 2012. About four in ten (41.7%) said they expect fewer numbers of contractors by the end of the year. However, this is an improvement over the 2011 and 2010 surveys when 53% and 73.4% of executives, respectively, said they expected fewer contractors by the end of the year.