ConstructConnect announced that September’s volume of construction starts, excluding residential activity, was $42.8 billion. The month-to-month percentage change vs. August was an outsized +31.5% (or plus nearly one-third). The big improvement in the latest period was thanks to go-aheads for three mega projects combining for a total of $17 billion.

The three extraordinary projects were an Exxon Mobil petrochemical plant in Texas ($10 billion categorized as industrial); the new Delta Airlines Terminal at LaGuardia Airport in New York ($4 billion categorized as civil/engineering); and the Atlantic Sunrise natural gas pipeline in Pennsylvania ($3 billion, also in the civil/engineering type-of-structure category).

Compared to the same month of last year, this September was +43.4%. Relative to January-to-September of 2016, 2017’s year-to-date starts through the first nine months have been +9.4%.

The starts figures throughout this report are not seasonally adjusted (NSA). Nor are they altered for inflation. They are expressed in what are termed ‘current’ as opposed to ‘constant’ dollars.

Nonresidential building’ plus ‘engineering/civil’ work accounts for a larger share of total construction than residential activity. The former’s combined proportion of total put-in-place construction in the Census Bureau’s August report was 57%; the latter’s was 43%.

ConstructConnect’s construction starts are leading indicators for the Census Bureau’s capital investment or put-in-place series. Also, the reporting period for starts (i.e., September 2017) is one month ahead of the reporting period for the investment series (i.e., August 2017.)

The total number of U.S. construction jobs rose by 8,000 in September according to the latest Employment Situation report from the Bureau of Labor Statistics (BLS). The monthly average gain in on-site jobs to date in 2017 has been a little faster than during the same January-to-September period of last year, +14,000 compared with +11,000. The NSA unemployment rate in the ‘hard hat’ sector stayed the same in September as in August, at 4.7%. A year ago, in September 2016, construction’s jobless level had been a bit more elevated, at 5.2%.

The September labor survey results, both ‘payroll’ and ‘household’, were based on conditions that prevailed nearly simultaneous with Hurricanes Harvey and Irma laying severe beatings on southern Texas and much of Florida. Rebuilding efforts during the remainder of 2017 will surely put additional pressure on labor and material supplies. U.S. year-over-year construction employment, at +2.7%, is already proceeding at about twice the pace of the nation’s total jobs performance, +1.4%. Also notable is the current strong showing of ‘architectural and engineering services’ jobs, +3.4%. Design activity points the way to subsequent work levels in the field.

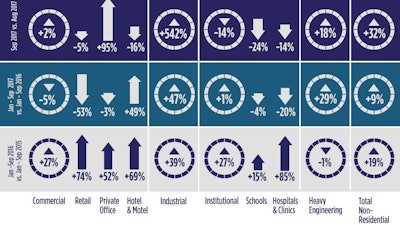

September’s month-to-month (m/m) overall starts increase (+31.5%) resulted from a huge jump in industrial (+542.4%), a solid increase in heavy engineering/civil (+18.3%) and a modest uptick in commercial (+2.1%). Institutional was the only major subcategory to falter (-14.2%).

As for the +43.4% September-2017-over-September-2016 (i.e., y/y) gain, industrial’s impact (thanks to Exxon Mobil) was even greater (+1049.5%), with engineering ahead mightily as well (+64.6%). Commercial (-15.3%) and institutional (-14.3%) stood in the shadows.

Year-to-date (ytd) total starts (+9.4%) were led by industrial (+46.6%) and engineering (+29.2%), with institutional almost neutral (+1.2%) and commercial in the doldrums (-5.1%).

Within engineering, the ‘road/highway’ segment (with a 38% share so far in 2017) figures most prominently. In September, street starts were -16.8% m/m and -16.3% y/y, but +12.9% ytd. ‘Water/sewage’ work is second most important in the civil category (with a 22% slice ytd) and in the latest month, it was -22.0% m/m and -10.5% y/y, but +12.0% ytd. The ‘green-lighting’ of airport construction, however, was where the most spectacular lift-off occurred: +410.7% m/m; +718.8% y/y; and +122.3% ytd. Delta’s new terminal at LaGuardia was the catalyst.

‘Bridge’ starts have also been tracking well. While they were -28.6% m/m, they were an upbeat +50.7% y/y and +46.0% ytd. Additionally, ‘miscellaneous civil’ (on account of new pipeline capacity in Pennsylvania to deliver natural gas from shale rock deposits) turned in a full set of good percentage changes in the latest month: +25.6% m/m; +255.5% y/y; and +73.4% ytd.

More than half (54%) of institutional starts to date this year have been provided by ‘schools/colleges’. Unfortunately, educational work has not maintained a passing grade: -24.3% m/m; -5.7% y/y; and -3.9% ytd. ‘Hospital/clinic’ starts, next most important within institutional (a 14% share) have similarly failed to impress: -14.1% m/m; -68.6% y/y; and -20.2% ytd.

Ranking first among ‘niches’ within commercial so far this year has been ‘hotel/motel’ work (with a 22% share). While that subgrouping had a rocky September both m/m (-15.6%) and y/y (-15.0%), it stayed encouragingly buoyant ytd (+48.8%). Meanwhile, the percentage changes for ‘private offices’ (20% of commercial) in the latest month, ran the gamut from a big increase m/m (+95.4%); to neutral ytd (-2.5%); and steeply down y/y (-31.7%). Finally, ‘retail/shopping’ has had commercial’s toughest time in 2017: -4.7% m/m; -28.7% y/y; and -52.6% ytd.

The ‘retail’ and ‘private office building’ curves have been heading down sharply for a considerable while now. ‘Schools/colleges’ and ‘hospitals/clinics’ have also been descending, but with more decorum. Some of the engineering subcategories, though, have been displaying resilience, with ‘bridges’ soaring and ‘miscellaneous power’ returning to a steady position.

Worker compensation throughout the U.S. economy appears to be gradually climbing. Construction workers fared better, but only by the tiniest of degrees, +3.0% both hourly and weekly. Leaving out supervisory personnel the economy-wide increases were +2.5% both hourly and weekly. Construction workers achieved the same weekly, +2.5%, but had happier results hourly, +3.1%.

The value of construction starts each month is summarized from ConstructConnect’s database of all active construction projects in the U.S. Missing project values are estimated with the help of RSMeans’ building cost models.

ConstructConnect’s nonresidential construction starts series, because it is comprised of total-value estimates for individual projects, some of which are ultra-large, has a history of being more volatile than many other leading indicators for the economy.