Geopolitical tensions and Indonesia’s trade policy continue to impact costs in the North American Construction Industry, according to IHS and the Procurement Executives Group (PEG).

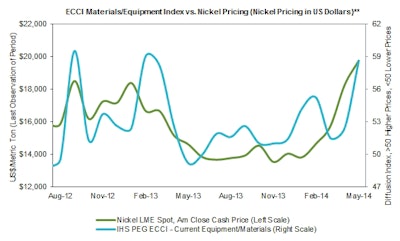

Indonesia’s decision in January to move forward with an export ban on unprocessed mineral ore always posed an upward risk to nickel prices, a key ingredient in stainless steel and alloy products. However, once combined with the threat of focused sanctions on Russian industry — the second largest producer of the refined metal — the risk premium has resulted in a sharp upward movement in nickel prices. This in turn has become a major concern reported by respondents to the latest survey of the North American construction industry.

Survey Methodology

The IHS PEG Engineering and Construction Cost Index (ECCI) is based on data independently obtained and compiled by IHS from the procurement executives of leading engineering, procurement and construction firms. The headline index tracks industry-specific trends and variations, identifying market-turning points for key projects, and is intended to act as a leading indicator for wage and material inflation specific to this industry.

Each survey response is weighted equally for every $2 billion in spending in North America. Respondents are asked whether prices — either actual paid transactions or company-informed transactions — during the current month for individual materials, equipment, and regional subcontractor rates, were higher, lower or the same as the prior month.

Respondents are then asked for their six-month pricing expectations among these same subcategories. The results are compiled into diffusion indexes, in which a reading greater than 50 represents upward pricing strength and a reading below 50 represents downward pricing strength.

The current ECCI headline index registered 57.6% in May, up 5.2% from April. Both the ECCI’s subcomponents — the materials/equipment index and the subcontractor labor index — also moved higher, establishing a consistent picture on the two fronts.

Broad-based Increase in Material Prices

The materials/equipment component of the ECCI jumped to 58.6% in May, from 52.4% in April. The upward move was broad based, with all 12 subcomponents now showing rising prices for the first time since March 2013. Copper-based wire and cable, pumps and compressors and transformers rebounded sharply, showing the greatest increases in May after registering falling prices in April. Alloy steel pipe posted the strongest reading of any component in May, reflecting concerns that the upward pressure in nickel prices would be passed along.

“Nickel prices have risen by over 50% since the start of the year. Profit-taking spiked the price recently, but it is the supply picture that is providing the bulk of the upward pressure,” said Jason Kaplan, senior manager of the Pricing and Purchasing Service at IHS. “The Indonesian ore export ban, other production outages, and uncertainty about how the Russian-Ukrainian conflict will affect supply continue to provide the upward pressure and will ensure prices remain high in the near future.”

By definition as a diffusion index, the rise in the materials/equipment component of the ECCI does not necessarily indicate that prices are strengthening, but rather that more survey respondents are experiencing higher prices in the North American construction industry.

Elevated Labor

The other segment of the ECCI, the subcontractor labor index, also continued on an upward trajectory, rising to 55.1% in May, up 2.8% from April. “The concern continues to be the tightness of qualified welders and electricians, particularly in the US Gulf Coast region due to an upcoming strong investment cycle in petrochemical and LNG facilities,” said Laura Hodges, director of the Pricing and Purchasing Service at IHS.

To learn more about the new IHS PEG Engineering and Construction Cost Index or to obtain the latest published insight, please visit: www.ihs.com/ecci