New home sales in the U.S. fell 0.6% in February, while existing home sales rebounded 3.0% but only partially offset a 3.2% drop the prior month. Sales for both are off to a disappointing start for 2018.

While the slow start may simply be the result of lingering winter weather across much of the Northeast and Midwest, a more fundamental issue is the worsening affordability problem across more of the country.

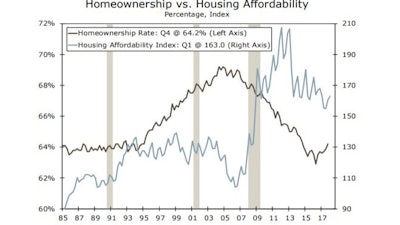

The National Association of Realtors measures affordability by comparing the median price of an existing home with median household income and the prevailing conventional mortgage rate. The affordability index captures the typical family’s ability to afford to purchase the typical home and is reported as the share of income needed to qualify for a mortgage, assuming a 20% down payment. The current reading of 163 means that a family earning the median family income has 163% of the income necessary to qualify for a conventional loan covering 80% of a median priced home. From a historical perspective, that is a relatively high level of affordability.

Unfortunately, affordability is not evenly distributed across the country or across price points. Understanding the dispersion of housing affordability across geographies and price points is key to unraveling the mystery of why home buying is taking so long to gain traction.

Housing affordability is highest in the Midwest, at 206.1 in January, where job growth is the slowest; and the lowest in the West, at 114.0, where job growth is strongest. The Northeast and South are 170.8 and 168.0, respectively. Even this breakout oversimplifies the issue.

The past decade has seen a significant move back to major metro areas, particularly among younger households. Affordability in the fastest growing areas has deteriorated relative to the national and regional averages, which explains a large part of the slide in the share of consumers that feel now is a good time to buy a home.

(go to Wells Fargo Economics’ April Housing Chartbook . . . )