Middle market M&A transaction volume and value were both winners in 2015; however, data and sentiment show that we crossed the finish line running on fumes, as evidenced by slowing deal flow in Q4 and peaked valuations. Our discussions with business owners often include the topic of transaction activity. People often equate Wall Street M&A activity to what is happening on Main Street and in the middle market. The mega deals we see happening in the news are not necessarily indicative of what is happening in most of the business world, which resides in the middle market—especially the lower end of the middle market. That’s why it’s important to look at these two very different markets separately. Our firm’s research and expertise focuses on transactions with total enterprise value (TEV) of less than $250M.

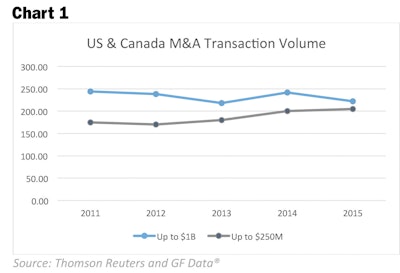

To illustrate the difference between Wall Street and Main Street trends, we look at deal volume from two perspectives, comparing M&A transaction volume of deals up to $1B (upper middle market) and up to $250M (lower middle market). When factoring in the larger transactions, the trend reveals that lower middle market deal volume in 2015 finished equal to or better than in 2014, but when factoring in upper middle market deal volume, 2015 finishes lower than in 2014.

Chart #1, Above

Regardless of whether it’s Wall Street or Main Street, M&A activity is still fueled by underlying macro-economic indicators, which were good in 2015. The unemployment rate fell to 5.0 percent at the end of 2015. Consumer sentiment finished the year at a decent 92.6, up from last summer’s low 87.2 during the equity market turmoil. External factors, including slower foreign demand, weighed on overall GDP growth, which increased 1.8 percent in 2015—down from 2.4 percent growth in 2014 and 2.2 percent growth in 2013. The sharp decline in oil prices was a major economic development in 2015, and estimates are that those lower oil prices directly boosted real GDP growth by 0.2 percentage point during 2015, despite adverse impacts on domestic energy producers and manufacturers that sell to the energy sector.

Pursant also looks at a number of other, more direct indicators of strategic transaction activity, including business spending and construction spending. Both of these indicators had favorable readings in 2015, supporting the theory that the US remains an economic oasis when compared to economically challenged Europe and Asia. Fixed investment rose 2.7 percent over the course of the year.

We also review interest rate trends as a leading indicator. Because of sustained economic improvement in 2015, the Federal Reserve decided to move forward with the federal funds rate increase in December. Fed Chairman Janet Yellen stated that future increases will be cautious and gradual, knowing that tightening too much or too soon could choke off the economic recovery. This increase could mark a turning point by altering the current very low cost of capital, which could then initiate downward pressure on M&A volume and valuations in 2016. Some have said that this already has begun to happen.

Valuations for 2015 finished the year very strong. The low cost of capital, limited organic growth options and favorable domestic economic tailwinds increased buyers’ valuation appetites in 2015.

Chart #2 shows that frothy multiples were the theme for the lower middle market in 2015. The data shows that companies throughout the lower middle market have managed to grow valuations in 2015, with the exception of companies in the $50M-$100M TEV range (which is likely a data anomaly).

Chart #2, Above

[Pull Quote]

For most businesses, valuation is typically expressed in the form of a multiple of EBITDA (earnings before interest, taxes, depreciation and amortization)—a measurement of a company’s ability to generate cash flow. EBITDA figures also serve as a barometer of the company’s health and performance. Multiples of EBITDA vary greatly depending on a company’s risk profile, the markets in which it operates and the likelihood of continued returns.

The Story on Quality Premiums

Chart #7 illustrates that companies with above average financial characteristics (“W/QP”) garnered higher multiples at all levels in 2015 compared to companies without that premium. The “quality premium” is reserved for companies that have above average financial characteristics, defined as TTM EBITDA margins and revenue growth each exceeding 10 percent. Approximately two-thirds of companies have fallen into this category in 2015, up from approximately 50 percent in 2014

Chart #7, Above

As part of our 2015 year-end review, here is added insight into many of the most common deal related questions:

Why are people selling?

Chart #4 shows that the majority of people continue to sell due to retirement. With many of the aging baby-boomers still working, this number is expected to grow in the coming years. The second most common reason is ownership fatigue—in fact, this is the most common reason for clients of our firm. This may be due in part to the fact most of our clients have companies that are valued at less than $250M and with smaller businesses, more of the burden of running a business falls squarely on the shoulders of the owners.

Chart #4, Above

When I am ready to sell, who are the buyers?

Chart #5 shows that who buys your business largely depends on its size. If you have a business that is valued at less than $500k, the odds are that it will be acquired by an individual. Large strategic and financial buyers stand to gain very little by buying a small business. The modest amount of revenue growth they will gain can be acquired organically at a much lower cost. You will also notice that financial buyers don’t even enter the picture until total enterprise value (TEV) exceeds $5M. Strategic buyers are available at virtually all price points, but less so at the sub $500k value level.

Chart #5, Above

Is it a buyer’s or seller’s market?

Chart #6 shows that the answer to that question is, “it depends.” The primary reasons for the difference in who has the upper hand are risk and supply. There is an abundant number of small businesses in North America, most of which are fraught with risk associated with ownership dependence and customer concentrations. As a business grows, it develops layered management teams; the owner is less critical to the sustainability of the business and the business becomes less dependent on key customers. This results in lower risk and short supply (because few people can pull this off), so demand is strong for businesses with this profile.

Chart #6, Above

Deep Dive – Debt Recapitalization

In our Q4 2014 edition of the Pursant M&A Insider, we highlighted debt and equity recapitalizations as examples of liquidity options for business owners. In our Q1 2015 edition, we discussed equity recapitalizations in more detail. In this edition, we take a deep dive into debt recapitalizations.

As a reminder, a recapitalization (recap) is a financing activity resulting in a change to a company’s capital structure. The purpose is to shift the business and economic risk from the existing ownership to an outside party or parties.

Debt recapitalizations are accomplished through raising senior and/or subordinated debt. Senior debt refers to debt that is in a first-lien position such that in the event of a default or liquidation, the senior lender has first priority in recouping its investment. Senior debt providers are often commercial banks. Subordinated debt, which is commonly referred to as mezzanine or junior debt, is second in line to senior debt, which makes it a higher risk investment for the lender and therefore carries a higher interest rate than senior debt. Chart #3 shows average interest rates for both senior and junior debt capitalizations in 2014 and 2015, and illustrates that the very low cost of debt is one of the drivers of recap activity. These rates are averages with larger amounts having lower rates and smaller amounts having higher rates.

Chart #3, Above

In a debt recapitalization, the Company secures outside financing generally to facilitate a capital distribution to the business owners (e.g. dividend) or to generate capital for other strategic purposes (e.g., acquisitions). Debt recapitalizations allow business owners to retain 100% ownership of the Company and, compared to raising capital through other channels, are generally executed efficiently with minimal disruption to business operations. Another key attribute of debt recapitalizations is that they are sources of “cheap money.” Creditworthy Companies often find that the cost of debt is significantly lower than the cost of equity. Furthermore, the interest expense is tax-deductible.

While debt recapitalizations have many appealing attributes, business owners need to ensure that such transactions are properly understood and evaluated. One of the most significant considerations is the Company’s ability to service debt obligations. The need to service these obligations increases a Company’s vulnerability, as challenges related to both company specific and market/economic events can be unforeseen. To mitigate this exposure, it is critical for business owners to evaluate the ability to service the new debt principal and interest obligations, and to do so by modeling a variety of different scenarios (stress tests), assumptions and criteria.

Other key considerations regarding debt refinancing include (i) new or enhanced transparency and financial reporting requirements; (ii) the requirement to implement additional financial and business process controls; and (iii) adherence to covenants which establish rules and parameters related to business activities and cash usage. It is critical that owners plan appropriately to ensure that personnel and business operations are equipped absorb any new responsibilities required.

With proper planning and consideration, debt recapitalization can be a very attractive solution designed to meet liquidity and/or capital needs of your business. As with any key strategic endeavor, the key is proper diligence to ensure that all possible benefits are realized and all risks are mitigated.

Pursant’s Top 10 Predictions for 2016

Strong but lower transaction activity unless the economy softens and rates increase too much

- Stabilization to slightly lower valuations, especially if Fed moves rates up a full point or more

- Emergence of more strategic buyers

- 2-4 additional Fed rate increases

- Improvement of access to bank debt for small business

- Continued demand for alternative lending

- Sustained demand for quality earnings

- Emergence of Baby Boomers— finally

- Increase in the number of companies Stress-Testing, Optimizing and Exit Planning

- The potential for global events to derail any and all of the above

We have seen that business owners are increasingly receptive to the idea of a sale or partial liquidity event (see this quarter’s Debt Recapitalization topic). When the broader market has tail winds favoring the seller, when they have a healthy business and when they are personally ready, owners are seeing that they need to seize the opportunity and monetize the value of their businesses.

For the sellers, this optimal timing will continue to align well with buyers’ appetites and continued desire for acquisitive growth, due to the fact that organic growth percentages are generally low. As we have stated in the past, acquisitions will continue to emphasize strategic fit, synergies and the need to acquire good people in the process. Creative deal structures will address these criteria accordingly. Buyers will continue to demand thorough and professionally prepared information, further supporting the need for owners to put their businesses through a corporate stress test.

Pursant helps business owners grow the value of their companies and maximize that value in a liquidity event, partial sale or complete exit. Our Investment Banking, Financial Services and Strategic Advisory business units use a deep immersion process, our expansive networks and experience as owners/operators to successfully optimize operations and manage strategic transactions — vital, integrative initiatives for which our clients may not have the time, manpower or expertise. To learn more about how Pursant can help you, contact Mark Herbick at [email protected], call 847.229.7000 or visit www.Pursant.com.

Information provided by Pursant, LLC, GF Data® and Thomson Reuters® in this report may not be used in work product or republished in any format without written permission of Pursant, LLC, GF Data® and Thomson Reuters®.

![Lee Boy Facility 2025 17 Use[16]](https://img.forconstructionpros.com/mindful/acbm/workspaces/default/uploads/2025/09/leeboy-facility-2025-17-use16.AbONDzEzbV.jpg?ar=16%3A9&auto=format%2Ccompress&dpr=2&fit=crop&h=135&q=70&w=240)