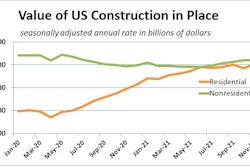

- Construction project optimism is high for 2022

- Consumer demand remains high

- Supply chain still constrained

- Raw materials inventories increasing

- Manufacturing commodity prices increasing

Prices are too high and inventories are too low, but overall, the economy and the manufacturing sector are in growth mode.

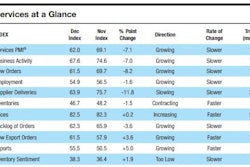

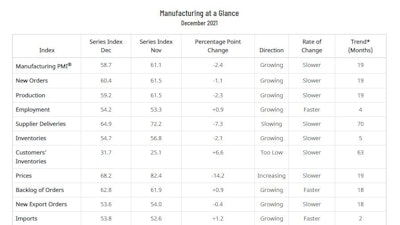

Economic activity in the manufacturing sector grew in December, with the overall economy achieving a 19th consecutive month of growth, according to the latest Manufacturing ISM Report on Business, out this week.

The report was issued by Timothy Fiore, chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee. The Manufacturing PMI, or the Purchasing Managers’ Index, is a set of economic indicators based off surveys of private-sector companies.

“The December Manufacturing PMI registered 58.7%, a decrease of 2.4 percentage points from the November reading of 61.1%. This figure indicates expansion in the overall economy for the 19th month in a row after a contraction in April 2020,” Fiore says.

Many COVID-19 issues are still in play, impacting the manufacturing sector.

“The U.S. manufacturing sector remains in a demand-driven, supply chain-constrained environment, with indications of improvements in labor resources and supplier delivery performance,” he says. “Shortages of critical lowest-tier materials, high commodity prices and difficulties in transporting products continue to plague reliable consumption. Coronavirus pandemic-related global issues — worker absenteeism, short-term shutdowns due to parts shortages, employee turnover and overseas supply chain problems — continue to impact manufacturing. However, panel sentiment remains strongly optimistic, with six positive growth comments for every cautious comment, down slightly from November.”

ISM

ISM

2022 Expectations

ISM’s Semiannual Economic Forecast, released in December, indicates a strong 2022 performance expectation in terms of revenue growth and profitability. Demand expanded, with the New Orders Index growing, supported by continued expansion of new export orders, Customers’ Inventories Index remaining at a very low level and Backlog of Orders Index staying at a very high level.

“Construction projects for 2022 and 2023 look very strong for us,” a survey respondent in the nonmetallic mineral products sector reports.

Consumption (measured by the Production and Employment indexes) grew during the period, with a combined negative 1.4-percentage point change to the Manufacturing PMI calculation. The Employment Index expanded for a fourth straight month, with some indications that ability to hire is improving, though somewhat offset by the continued challenges of turnover and backfilling. Inputs — expressed as supplier deliveries, inventories and imports — continued to constrain production expansion, but there are clear signs of improved delivery performance. The Supplier Deliveries Index again slowed while the Inventories Index expanded, both at a slower rate. In December, the Prices Index increased for the 19th consecutive month, at a slower rate (a decrease of 14.2 percentage points), indicating that supplier pricing power continues to rise, but to a lesser degree.

“All of the six biggest manufacturing industries — chemical products, fabricated metal products, computer and electronic products, food and beverage, transportation equipment and petroleum and coal products, in that order — registered moderate-to-strong growth in December.

Hiring remains a hiccup for the manufacturing sector.

“Manufacturing performed well for the 19th straight month, with demand and consumption registering month-over-month growth,” Fiore says. “Meeting demand will remain a challenge, due to hiring difficulties and a clear cycle of labor turnover at all tiers. For the second month in a row, business survey committee panelists’ comments suggest month-over-month improvement on hiring, offset by backfilling required to address employee turnover. Supplier delivery rate improvement was indicated by the Supplier Deliveries Index softening in December.”

Transportation networks, a harbinger of future supplier delivery performance, are still performing erratically; however, there are signs of improvement, he says.

The 15 manufacturing industries reporting growth in December, in the following order, are: apparel, leather and allied products; furniture and related products; textile mills; plastics and rubber products; machinery; nonmetallic mineral products; miscellaneous manufacturing; chemical products; electrical equipment, appliances and components; fabricated metal products; computer and electronic products; food, beverage and tobacco products; transportation equipment; primary metals; and petroleum and coal products. The three industries reporting a decrease in December compared to November are: wood products; printing and related support activities; and paper products.

“Costs for steel seem to be coming down some,” a survey respondent in the machinery sector reports. “We have seen a little relief on steel prices, but they are still very high. Overall performance by suppliers has improved. On-time deliveries have improved.”

Commodities

The following commodities are up in price (in parentheses is the number of months prices have been increasing): adhesives and paint; aluminum* (19); capacitors; corrugate (15); corrugated packaging (14); diesel fuel (12); electrical components (13); electronic components (13); freight (14); labor — services; labor — temporary (8); logistics services; lubricants; lumber; natural gas* (6); nylon (3); ocean freight (13); packaging supplies (13); printed circuit boards (pcbs); resin based products (11); resistors; rubber based products (5); semiconductors (11); silicone (2); steel* (17); steel — galvanized; steel — stainless (14); and steel products* (16). An * means the commodity has gone up and down in price.

The following commodities are down in price: aluminum* (2); crude oil; ethylene; natural gas*; polyethylene; propylene; steel* (2); and steel — hot rolled (2).

The following commodities are short supply: aluminum (2); copper products; electrical cables; electrical components (15); electronic components (13); labor — temporary (8); plastic resins — other (10); rubber based products; semiconductors (13); and steel (13).

ISM

ISM

Production

The Production Index registered 59.2% in December, 2.3 percentage points lower than the November reading of 61.5%, indicating growth for the 19th consecutive month.

“Four of the top six industries — chemical products; computer and electronic products; food, beverage and tobacco products; and transportation equipment — expanded at moderate-to-strong levels. Raw material and labor shortages remain a constraint to production growth, as suppliers continue to struggle. Panelist sentiment on labor and material shortages improved for a second month, albeit at a low level,” says Fiore.

An index above 52.1%, over time, is generally consistent with an increase in the Federal Reserve Board’s Industrial Production figures.

The 10 industries reporting growth in production during the month of December, listed in order, are: furniture and related products; plastics and rubber products; textile mills; paper products; chemical products; machinery; computer and electronic products; food, beverage and tobacco products; transportation equipment; and miscellaneous manufacturing. The four industries reporting a decrease in December are: apparel, leather and allied products; wood products; fabricated metal products; and primary metals.

ISM

ISM

Employment

ISM’s Employment Index registered 54.2% in December, 0.9 percentage point above the November reading of 53.3%.

“The index reported a fourth consecutive month of expansion. Of the six big manufacturing sectors, three (fabricated metal products; chemical products; and computer and electronic products) expanded. Survey panelists’ companies are still struggling to meet labor-management plans, but for a fourth month, there were modest signs of progress: A stable share of comments (7% in both December and November, compared to 5% in October) noted greater hiring ease. An overwhelming majority of panelists indicate their companies are hiring or attempting to hire, as 85% of Employment Index comments were hiring focused. Among those respondents, 37% expressed difficulty in filling positions, a decrease from November. A high level of comments regarding turnover rates (backfills and retirements) in December continued a trend that began in August,” says Fiore.

An Employment Index above 50.6%, over time, is generally consistent with an increase in the Bureau of Labor Statistics (BLS) data on manufacturing employment.

Of 18 manufacturing industries, eight industries reported employment growth in December, in the following order: apparel, leather and allied products; nonmetallic mineral products; electrical equipment, appliances and components; plastics and rubber products; machinery; fabricated metal products; chemical products; and computer and electronic products. The five industries reporting a decrease in employment in December are: textile mills; wood products; paper products; food, beverage and tobacco products; and miscellaneous manufacturing.

ISM

ISM

Supplier Deliveries

The delivery performance of suppliers to manufacturing organizations was slower in December, as the Supplier Deliveries Index registered 64.9%, 7.3 percentage points lower than the 72.2% reported in November. Five of the six top manufacturing industries — fabricated metal products; food, beverage and tobacco products; computer and electronic products; chemical products; and transportation equipment — reported slowing deliveries.

“Deliveries slowed at a slower rate compared to the previous month,” Fiore says. “The index continues to reflect suppliers’ difficulties in meeting panelist companies’ demand, but for the second straight month, supply chain performance is moving toward a more appropriate balance with demand. Capital expenditure lead times continue at modern-era records. Production materials lead times registered a 5% improvement from the prior month but remain at near-record levels. The Supplier Deliveries Index, Prices Index and material lead times softening in November and December indicate progress against the supply/demand imbalance.”

A reading below 50% indicates faster deliveries, while a reading above 50% indicates slower deliveries.

Fourteen of 18 industries reported slower supplier deliveries in December, in the following order: apparel, leather and allied products; textile mills; nonmetallic mineral products; furniture and related products; miscellaneous manufacturing; paper products; plastics and rubber products; fabricated metal products; primary metals; food, beverage and tobacco products; machinery; computer and electronic products; chemical products; and transportation equipment. The two industries reporting faster supplier deliveries in December as compared to November are: wood products; and electrical equipment, appliances and components.

ISM

ISM

Inventories

The Inventories Index registered 54.7% in December, 2.1 percentage points lower than the 56.8% reported for November.

“Manufacturing inventories continued to expand but at lower levels, as end-of-year working capital targets are likely a cause of softening in the index. Also, the index somewhat reflects an improved flow of raw materials to factories,” says Fiore.

An Inventories Index greater than 44.5%, over time, is generally consistent with expansion in the Bureau of Economic Analysis (BEA) figures on overall manufacturing inventories (in chained 2000 dollars).

The 10 industries reporting higher inventories in December, in the following order, are: apparel, leather and allied products; machinery; miscellaneous manufacturing; chemical products; furniture and related products; electrical equipment, appliances and components; fabricated metal products; plastics and rubber products; transportation equipment; and computer and electronic products. The four industries reporting a decrease in inventories in December are: printing and related support activities; paper products; food, beverage and tobacco products; and primary metals.

Customer Inventories

ISM’s Customers’ Inventories Index registered 31.7% in December, 6.6 percentage points higher than the 25.1% reported for November, indicating that customers’ inventory levels were considered too low.

“Customers’ inventories are too low for the 63rd consecutive month, a positive for future production growth. For 17 straight months, the Customers’ Inventories Index has been at historically low levels,” says Fiore.

No industries reported higher customers’ inventories in December.

ISM

ISM

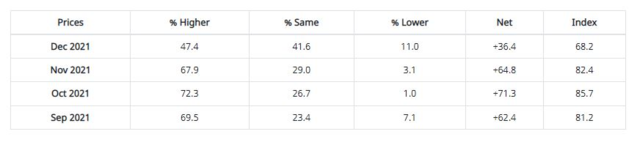

Prices

The ISM Prices Index registered 68.2%, a decrease of 14.2 percentage points compared to the November reading of 82.4%, indicating raw materials prices increased for the 19th consecutive month, at a slower rate in December.

“Price increases appear to be slowing,” a survey respondent in fabricated metal products says. “Lead times are shrinking slowly, and inventories are growing. I hope we have reached the top of the hill to start down a gentle slope that lets us get back to something that resembles normal.”

This is the 16th month in a row that the index has been above 60%.

“Aluminum; corrugate and packaging materials; electrical and electronic components; energy; lumber; freight and some steels continue to remain at elevated prices due to product scarcity amongst high demand,” says Fiore.

A Prices Index above 52.7%, over time, is generally consistent with an increase in the Bureau of Labor Statistics (BLS) Producer Price Index for Intermediate Materials.

In December, 16 industries reported paying increased prices for raw materials, in the following order: apparel, leather and allied products; textile mills; furniture and related products; paper products; primary metals; miscellaneous manufacturing; machinery; computer and electronic products; chemical products; food, beverage and tobacco products; nonmetallic mineral products; fabricated metal products; transportation equipment; wood products; electrical equipment, appliances and components; and plastics and rubber products. Only one industry, petroleum and coal products, reported paying decreased prices for raw materials.

ISM

ISM

New Export Orders

ISM’s New Export Orders Index registered 53.6% in December, down 0.4 percentage point compared to the November reading of 54%.

“The New Export Orders Index grew for the 18th consecutive month, at a slightly slower rate. Of the six big industry sectors, four (food, beverage and tobacco products; computer and electronic products; chemical products; and transportation equipment) expanded. New export orders activity was a contributor to the New Orders Index continuing in strong expansion territory,” says Fiore.

The six industries reporting growth in new export orders in December, in the following order, are: plastics and rubber products; food, beverage and tobacco products; computer and electronic products; miscellaneous manufacturing; chemical products; and transportation equipment. The three industries reporting a decrease in new export orders in December are: textile mills; paper products; and machinery. Seven industries reported no change in exports in December as compared to November.

ISM

ISM

Imports

ISM’s Imports Index registered 53.8% in December, an increase of 1.2 percentage points compared to November’s figure of 52.6%.

“Imports expanded in December for the second consecutive month, in spite of continuing challenges with throughput at U.S. ports of entry. Overland transport challenges and container shortages continue to persist across the global supply chain, causing instability with import-level projections. Imports will continue to be challenged through the first half of 2022,” Fiore says.

The six industries reporting growth in imports in December, in the following order, are: furniture and related products; petroleum and coal products; computer and electronic products; food, beverage and tobacco products; machinery; and chemical products. The five industries reporting a decrease in imports in December are: nonmetallic mineral products; fabricated metal products; plastics and rubber products; transportation equipment; and miscellaneous manufacturing. Seven industries reported no change in imports in December as compared to November.

Buying Policy

Average commitment lead time for Capital Expenditures in December was 161 days, an increase of one day compared to November. Capital Expenditures lead times have increased in 10 of the last 12 months for a net increase of 20 days since January 2021 (141 days). Average lead time in December for Production Materials decreased by five days to 91 days. Average lead time for Maintenance, Repair and Operating (MRO) Supplies was 48 days, up four days compared to November.