Now’s the time to get your act together so you can quickly close out 2016 in January and not June 2017. I think we all know that the more delays in your ability to know what is going on in your business, the less time you have to make corrections in the New Year. You would be amazed how many company owners believe they had a good year only to find out (six to nine months after the fact) that they did not.

I’m speaking from experience here as a CPA and ex-Audit Partner. I know that companies that have control of their numbers are able to adapt solutions almost immediately at the beginning of the New Year, as opposed to those who don’t find out that they have a problem until June, leaving only six months of “solution” time in the current year. There’s a big difference!

There is no question that keeping the books straight is important, along with appropriate current key performance indicators (KPIs) that keep you informed about operating results and cash flow. Most industry-specific systems provide this type of data, but require quality data to generate meaningful reports. Garbage-in/garbage-out reports prove to be weak in terms of assisting with decision making.

One misconception we deal with when it comes to “keeping the books straight” is the belief that all this internal auditing has to be done at year end. Not true. You save time by spreading the audit process over the entire year (as time permits), and you then make adjustments and move on to other areas to review. As long as you review all major areas at least once a year, analyze the results, correct the mistakes and change procedures to eliminate the “problems,” eventually your house will automatically provide the data you need to run your business.

Some areas require more than one review a year. These would be the cash balance, AR collections, WIP billings and expenses, equipment repairs, overtime and AP. These categories cover the bulk of your exposure. If you keep these areas under control and have adequate cash flow to pay your bills, you can reasonable rely on your KPIs and other reports to provide correct data.

I would suggest this review take place quarterly with the entire management team present to discuss issues noted and to assign accountability to correct the various issue that come up.

Get Comfortable with Cash Flow

Cash flow and cash balances are the key to being able to sleep nights. Thus, this is where your time and effort should be devoted.

First, you must have a daily cash report that reflects (in a monthly report) the daily cash movement in terms of AR collections, bank loan receipts and other cash receipts, as well as key expense items such as field payroll, job expenses, sales and in-house employee payroll, overhead expenses, bank loan prepayments and all other G&A expenses. This is a simple report to maintain once you get used to the format; and, after a while, you will get comfortable with the monthly cash flow as well as your annual cash flow movements. Believe me when I say, once you’re comfortable with your cash flows, life gets a lot simpler.

There’s one caveat to add at this point, and it deals with a subject discussed previously, which is to keep in mind that a higher level of sales requires capital to support it. Remember the Growth Potential Index discussed a few months ago (ForConstructionPros.com/12250030)? I want to caution you to properly plan out anticipated revenue growth to ensure your cash position can handle the higher of level of disbursements required from the new work. It’s easy to believe cash flows are positive and will stay that way when in fact they won’t if you add significant new business. On the upside, if you have this daily cash report available, it will be easier to spot negative swings in cash before they get out of hand.

A way to put some of these ideas into practice is to hire some college students who major in accounting to build your reports for you and to audit the various suggested categories. Get someone with three years to go before graduation and you can make use of their talents and knowledge of your business to update the initial work for another three years. They can also help you to digitize your operation if that is of interest to you. These part-time helpers can work in the summer but also in December if you need to clean up accounts for year end.

Words to the Wise for 2017

Watch the debt load: The economy is kind of shaky so I would defer additional debt until you’re comfortable with your regional situation. Sorry to say this could take years. In fact, it would be a good thing if you can reduce your debt requirements, as well.

Maximize tax benefits in 2016: I’m suggesting to all the CEOs I work with to maximize their tax position in terms of depreciation deductions and other expenses for 2016 even if tax loss carryovers are created (which is what I’m looking for). In short, I know what these deductions are for 2016, but have no idea what they will be in 2017.

For example, I’m using both Section 179 and bonus depreciation so that if there is a carryover I know I will be able to use it in 2017. A tax law change in 2017 could limit or change tax depreciation charges with a negative impact on cash flow. This is an easy tax management play to make in an environment where there is too much talk about changing the tax code.

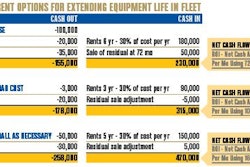

Consider getting an equipment appraisal: As I may have mentioned in the past, I like my book depreciation to be close to the orderly liquidation value (OLV) of that equipment. If your book depreciation does not reflect this value, I would consider a desktop appraisal to determine what your OLV really is. Again, the economy is the issue and I can see banks giving folks a hard time about their balance sheets, especially if they have no idea what their equipment fleet is worth.

It is also nice to know your OLV in case you want to sell some equipment off. And it will please your banker that you did it in the first place. A desktop appraisal is not an expensive proposition.

Cash is king: Enough said. Make sure you have positive cash flow and enough dry powder to take advantage of the really great opportunities that may pop up.

Garry Bartecki is the managing member of GB Financial Services LLP and a consultant to the Associated Equipment Distributors. He can be reached at (708) 347-9109 or [email protected].