Current construction costs fell again in February, said IHS Inc. and the Procurement Executives Group (PEG). The headline current IHS PEG Engineering and Construction Cost Index (ECCI) registered 41.3 this month, down from 43.3 in January. The headline index has been consistently below the neutral mark for 14 months.

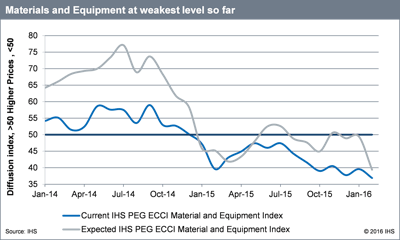

The current materials/equipment price index deteriorated once again, slipping from 39.6 in January to 36.9 this month. February's level is the lowest recorded since the survey began four years ago. All underlying material and equipment components showed falling prices except turbines, which showed prices unchanged. Compared to last month, fabricated structural steel had the largest drop and registered the lowest reading among equipment and materials. In addition, falling prices in almost all other categories demonstrate that weak pricing continues to migrate downstream.

“Finished steel prices – such as for plate and bar – have generally bottomed in North America and will soon see very mild increases,” said Jon Anton, director of steel analytics at IHS Pricing and Purchasing. “Fabrications prices tend to lag by one to two quarters, as steel must be purchased, cut and welded, then distributed. The bottom for fabricated metal should arrive in the second and third quarter of 2016, and very mild increases will be likely by the latter part of 2016.”The current subcontractor labor prices rose in February. However, the index retreated from 52.1 in January to 51.5 this month. The sub index has been above the neutral mark for the last four months, although still significantly lower than its historical average. In the United States, South and Midwest reported mostly neutral prices for subcontractor labor, while in Northeast and West, prices rose. Looking at Canada, the Western region recorded falling labor costs and in Eastern Canada labor costs were unchanged.

The six-month headline expectations index fell to 43.2 in February. The materials/equipment index dropped from 49.4 in January to 39.4, its lowest level since the beginning of the survey. Only ready-mix concrete came in above the neutral mark, while all other categories showed softer price expectations. For future subcontractor labor costs, expectations remained above the neutral mark at 52.0 and recorded a small drop compared to January. Respondents expect subcontractor labor costs to rise in the US Northeast, South and West. In the US Midwest, prices remained mostly unchanged. In both Western and Eastern Canada, labor prices are expected to fall.

Lower February figures demonstrate that capital expenditures continue to be challenged by falling oil prices. This was also evident in the survey comments, which highlighted continuing expectations for sluggish activity.