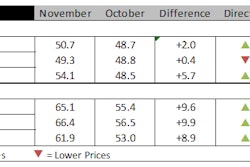

Construction costs rose for the second straight month, according to IHS Markit and the Procurement Executives Group (PEG). The headline current IHS PEG Engineering and Construction Cost Index registered 53.3, up from 50.7 in November, continuing the recovery after a 22-month slump in prices. Strength was evident in both labor and material markets.

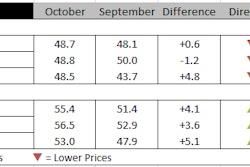

The current materials/equipment price index came in at 53.3 in December after two months of falling prices. Six of 12 categories tracked in the materials sub-index showed rising prices, three had falling prices, and prices remained unchanged in three categories. Pumps and compressors registered falling prices once again; prices have been falling for this category for almost 17 months. Exchangers had a similar profile, with prices only reaching the neutral mark this month after falling for 16 months. Weakness in these two categories indicates the recent strength in raw materials has yet to filter uniformly into intermediate and final goods.

"Notwithstanding the stronger readings of the past two months in the materials/equipment index, upstream commodity prices look exposed at the moment and poised for a correction,” said John Mothersole, director of research at IHS Pricing and Purchasing. “While we do see leverage becoming more evenly balanced between buyers and suppliers in 2017, we expect upstream commodity markets to reset in the months immediately ahead with prices pulling back at least temporarily to better reflect underlying fundamentals."

The current subcontractor labor index came in at 53.1 in December, slightly lower than the 54.1 November reading, but still presenting positive momentum. In the Northeast, Midwest and Southern United States, labor costs rose; in the West, costs remained the same as last month. Even areas affected by the downturn in energy markets are feeling the effects of a tightening labor market. In Canada, labor costs remained the same in both eastern and western regions.

The six-month headline expectations index recorded another month of increasing prices, with the index moving from 65.1 in November to a strong 68.9 in December. The materials/equipment index rose from 66.4 to 73.3, affirming widespread expectations of higher future prices. Every component showed rising prices; there were no expectations for softer materials prices. Sub-contractor labor price expectations came in at 58.7 in December, slightly lower than the November figure of 61.9. In the United States labor costs are expected to rise in every region. In Canada, labor costs are expected to remain the same.

In the survey comments, respondents have noted no supply shortages of materials. Proposal activity has registered an uptick in the recent months, and participants are showing increased optimism for 2017.

To learn more about the new IHS PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.