Table Detailing Nonresidential Construction Spending Growth Forecasts by Sector

The American Institute of Architects' outlook for spending on nonresidential building construction in 2012 and 2013 is not dampened by Europe's debt crisis, international political instability, a looming fiscal cliff of tax increases and spending cuts and a wildly gyrating stock market.

On the contrary, the AIA Consensus Construction Forecast Panel raised its projection for nonresidential construction spending to 4.4 percent this year—up from a forecast of 2.1 percent growth at the beginning of the year. The increase is predicted to accelerate to a 6.2 percent gain in 2013.

Despite the obstacles, nonresidential construction activity got off to a good start this year. An unusually mild winter in most parts of the Northeast and Midwest allowed many projects to progress faster than expected in the first quarter. As a result, commercial construction activity had increased about 4 percent through April, and about 10 percent from the same period a year ago. Gains in institutional buildings—largely education and healthcare—have been more modest recently.

The first quarter of 2012 was a welcome relief, given that 2011 was the third straight year of declines in nonresidential construction spending. But while 2009 and 2010 had seen double-digit declines, the drop in 2011 was much more restrained. Overall nonresidential construction spending for buildings declined about 4 percent last year. The downturn was a bit less for commercial and industrial facilities, and a bit more in the institutional categories.

However, the disappointing pace of growth in the broader economy has limited the need for additional nonresidential facilities. While, given the steep downturn, the economy might have been expected to snap back more sharply, this recovery has been uncomfortably restrained. After recording 3 percent real (inflation-adjusted) growth in 2010, national gross domestic product (GDP) growth slowed to 1.7 percent last year, and increased to only 1.9 percent in the first quarter of this year.

As a result of this modest economic growth, job growth has also been disappointing. During 2011, business payrolls increased an average of just over 150,000 per month nationally, a level likely to barely accommodate new entrants to the labor force without absorbing currently unemployed workers. The pace of job growth improved in the first quarter of this year, to 225,000 per month, before falling back to under 75,000 per month through April and May.

Additionally, there is some risk that the national economy will take a hit in early 2013 when several major federal tax and spending changes could take effect. The Bush-era tax cuts are slated to expire at the end of this year, as are a temporary cut in the Social Security payroll tax and extended unemployment benefits.

On top of this hit to consumers, 2013 is the first year of the $1.2 trillion in automatic spending cuts over the coming decade that resulted from Congress’ inability to agree to a deficit reduction plan. It’s also the year that the federal government will again approach the legal limit on federal borrowing. In the unlikely event that nothing changes to address this “fiscal cliff," the Congressional Budget Office has projected that the national economy could turn back into recession in the first half of next year.

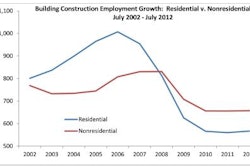

Housing not leading the construction upturn

Generally, an upturn in nonresidential construction activity is preceded by a housing recovery. During this cycle, however, housing has not contributed much to a construction turnaround, much less the national economic recovery. One of the main reasons for the weak housing sector is that many years of overbuilding led to a collapse in home prices. Between early 2006 and early 2009, home prices declined about 35 percent nationally, and have not shown significant improvement in most markets over the past three years.

The downturn in home prices coupled with a weak economy has created a record number of distressed properties. As of the end of the first quarter of this year, the Mortgage Bankers Association estimated that there were about 1.3 million homeowners with home mortgages 90 days or more past due (meaning that they were at risk of going into foreclosure), and an additional 2 million homeowners were at some stage of foreclosure. With this inventory of foreclosed homes in the pipeline, home prices are likely to remain under pressure for several more years.

Housing-market conditions, while fairly weak overall, vary significantly from market to market. Many of the traditionally fast-growing Sunbelt markets were left with significant excess inventories once the housing market crashed. This was especially true in areas of the Southeast and Southwest, where economic conditions significantly deteriorated. Many Northeast and Midwest markets saw less-significant house price declines because they were not as overbuilt when the market collapsed.

International opportunities become more limited

While the U.S. economy has been extremely weak, growth in many international economies has been significantly stronger, which has created export opportunities for many domestic businesses. As recently as 2010 and 2011, for example, economic growth in the United States was averaging less than 2.5 percent per year, just about equal to the growth rate of other advanced economies in the Eurozone, Japan, the United Kingdom, and Canada. Over this same period, however, emerging and developing economies were growing at almost three times this rate, paced by annual economic growth of almost 10 percent in China and almost 9 percent in India.

This pace of growth in developing economies likely cannot be sustained. In fact, an April 2012 forecast from the World Bank is projecting slower growth for emerging and developing economies for the remainder of 2012 and into 2013. Economic growth is projected to slow to under 6 percent per year in these economies, astronomical by current U.S. standards but a full percentage point below the pace of the past two years. China, India, Latin America, the Caribbean, and Central and Eastern Europe are expected to slow even more.

Additionally, debt problems are taking their toll on European economies. The World Bank is expecting a mild recession throughout the euro zone this year, with steeper declines in Italy and Spain, and only very weak growth in Germany and France. This anticipated slowdown in Europe, as well as in many emerging and developing economies, is expected to affect the domestic economy. The World Bank is projecting economic growth in the United States of 2.0 to 2.5 percent this year and next, thereby hampering a construction recovery.

Architecture firms seeing bumpy recovery

One of the best leading indicators of future construction activity is the current design activity at architecture firms. The AIA’s Architecture Billings index (ABI) measures monthly changes in design billings. Through the last two months of 2011 and the first three of 2012, design billings were slowly increasing. However, the April ABI score dipped slightly, and the May and June readings showed a steeper drop. This seesaw trend in design billings points to a slow and fairly modest recovery in construction activity.

The nonresidential sector that looks to have maintained the most momentum is commercial/industrial facilities. Architecture firms specializing in this sector had reported growth in billings for the second half of 2011 and the first four months of this year, with healthy growth for most of this period. With the recent downturn in the national index, the commercial/industrial component has seen slower growth, and has only very recently retreated into negative territory.

In contrast, firms concentrating on institutional facilities have seen much weaker design activity. Other than this past December and January, when the institutional design index was modestly positive, there have been steady declines in this sector for the past several quarters. Given the normal lag between design activity and construction activity for institutional buildings, this would indicate that there is unlikely to be much of any recovery in this sector this year.

A hesitant recovery emerges

In spite of all the headwinds facing the construction industry, the consensus is that there will be some gains in nonresidential construction spending in 2012, and stronger growth moving into 2013. All members of the AIA Consensus Construction Forecast Panel are expecting modest gains in nonresidential construction spending this year, with a consensus of growth between 4 and 5 percent. Likewise, all panelists are expecting the nonresidential construction upturn to continue into 2013, with spending gains to increase by 6 percent.

As seen with the ABI, stronger growth is anticipated for commercial and industrial facilities. All the panelists are expecting at least modest growth in spending for these facilities both this year and next. The consensus is for a 6 percent increase this year for commercial facilities and somewhat more for industrial facilities. Next year, growth for commercial buildings is projected to accelerate to 10 percent, with the industrial sector expected to see a more moderate gain of 8 percent.

The institutional upturn is forecast to be much more modest. Hardly any increase is expected this year, and the consensus for next year’s gain is just 3 percent. Healthcare is expected to generate most of the improvement in institutional spending, with this year’s 4 percent spending gains nearly doubling to just under 8 percent next year. Education construction, suffering from the dire fiscal situation of many state and local governments, is expected to see almost no growth this year or next.