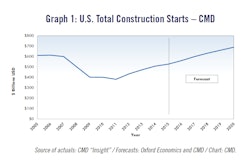

FMI reports that 2015 construction put in place will exceed earlier forecasts to end the year up around 10%. Construction growth is expected to slow to 8% in 2016, but will still be well ahead of GDP according to the Q4 FMI Construction Outlook.

Construction in 2016 is expected to reach $1.14 trillion in 2016, the highest total since 2007, unadjusted for inflation. As in 2015, one of the major challenges for the industry will be recruiting and training a talented workforce.

According to Chris Daum, FMI CEO, “2016 will challenge contractors’ growth plans, and there will always be new challenges to face. However, economic factors for construction are about the best we have seen since the recession, and we are looking for continued progress in 2016.”

The most notable improvements in growth have been for lodging (up 23%), office construction (up 19%), amusement and recreation (up 16%), and manufacturing (up 25%). The completion of the Panama Canal will mean a boost for manufacturing in Gulf Coast states. With little change since last quarter, manufacturing utilization rates were at 76.4% of capacity in October 2015, which has been consistent for the year. After two years of strong growth, manufacturing construction is expected to slow to a still-respectable level of 11% in 2016. The latest news expected to boost highway and transportation spending is the passing of a highway transit bill. According to ASCE, “The FAST Act provides $305 billion for highway, transit and railway programs.

Forecasts for key sectors

- Manufacturing – Manufacturing is currently the fastest-growing construction sector at 25% for 2015. However, we expect that rate to simmer in 2016 to 11%. Continued low energy prices will hold down capacity additions in the oil and gas sector, but help those relocating or expanding in other areas of manufacturing including the current boom in the petrochemical areas. Current fluctuations in the stock market and the future direction of the Chinese economy will be watched closely by those considering adding new manufacturing plants or relocating to the U.S. from offshore locations.

- Lodging – Lodging construction exceeded earlier estimates for 2015, and we now expect 23% growth for year-end 2015 and 17% for 2016 to $23.05 billion. The current pace is expected to slow as the supply catches up with demand and average daily rate growth slows. Currently, increased business travel and improving room rates combine to bring this market back from overbuilt pre-recession levels.

- Office – Office construction has demonstrated a remarkable comeback in the past two years and is expected to end 2015 up 19%. Much of the growth has come from an increase in employment, especially in high-tech job markets. We expect growth to carry over into 2016 and beyond, but at a slower rate.

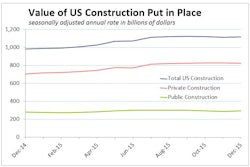

- Residential – Currently, nationwide there is more demand than supply for housing, as the current supply is at 5.5 months as of November 2015. That compares with a supply of 5.1 months in March and a supply of 12.2 months at the height of the recession in January 2009. The average monthly supply since 1963 is 6.1 months.