Stock-market handwringing since the first of the year has served as backdrop to a series of underwhelming construction-economy indicators released in recent weeks. For example:

- U.S. housing starts surprised everybody with a 3.8% tumble in January

- Private nonresidential construction spending capped a strong fourth quarter by dropping 2.1% in December

- The Architecture Billings Index slipped into contraction territory in January, signaling moderation in construction outlays nine to 12 months in the future

At World of Concrete February 2 through 5, Portland Cement Association VP and Chief Economist Ed Sullivan telegraphed a softening of his cement-consumption forecast for 2016. In November, he forecast 5% growth in the indicator of construction activity. He expects to shave his March reforecast by half to 1%, bringing the 2016 cement-consumption outlook down into the 4% to 4.5% range.

He’s keeping an eye on private nonresidential construction, which acts as a canary in the construction economy’s coal mine, and noted two more reasons for caution:

- Dodge Contract awards are down 25% over the past 8 months

- Cement Intensities (cement consumed per dollar of construction spending) declined 2.5% unexpectedly in 2015

“But look, the U.S. is creating well more than 200,000 jobs per month, and as long as that exists, the fundamentals supporting the construction economy are rock solid,” Sullivan said. "It could unravel, but it would take some time for that to happen, and I don't think that would be a 2016 issue."

He points out that consumer spending will bear the weight of the 2016 recovery, as weak global markets and a strong dollar impinge on U.S. exports.

As if on queue, retail sales posted a 0.2% rise in January, while core sales rose an impressive 0.6% for the month. Wells Fargo Economics analysis of the numbers says, “The strong pace of sales suggests that consumer spending remains robust enough to support modest economic growth,” even as the securities firm’s monthly economic outlook downwardly revised its forecast for first quarter GDP growth to just 1.0%.

Factors supporting continued construction-spending growth remain. Some keys emerging from the early-2016 melee:

- We’re starting from a strong 2015 performance, where the value of all construction put in place was 10.5% above 2014

- Soft January housing has shaken no residential construction forecasts

- Wells Fargo projects domestic demand to remain healthy and carry commercial real estate fundamentals

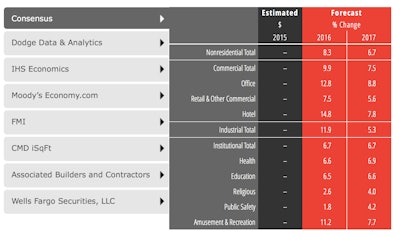

The American Institute of Architects’ 2016 Consensus Construction Forecast (a compiling of forecasts from seven key construction-industry economy watchers) is projecting that nonresidential construction spending will increase 8.3% this year. It’s important to note that this consensus was issued on February 11, well after financial markets had started to struggle, the December and full-year 2015 construction-put-in-place numbers were issued and

Some of the 2016 market segments AIA Consensus Forecasts:

- Commercial/industrial - 9.9%

- Office space - 12.8%

- Industrial facilities - 11.9%

- Healthcare facilities - 6.6%

- Education - 6.5%