As most equipment distributors know, some big changes to the tax code are scheduled for 2014, which both increase taxes payable on equipment sales and reduce the offsetting tax breaks historically available on replacement purchases.

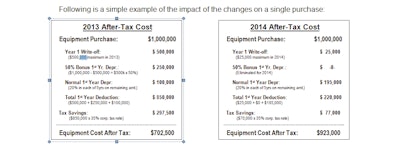

Tax reduction/deferral mechanisms that will disappear or see substantial reductions in 2014 include 50% bonus depreciation, which will disappear entirely, and the valuable Section 179 deduction, which will decrease from $500,000 in 2013 to $25,000 in 2014.

Section 1031 “like-kind exchange” treatment for sales of used/depreciated equipment may also be eliminated or substantially curtailed (it is not yet clear whether Congress will take this additional step, but “everything is on the table”). So, even some of the oldest and most commonly relied upon means of limiting taxes arising in connection with replacing equipment fleets may be eliminated.

In addition, the long-term capital gains tax rate (recently increased from 15% to 20%), plus a new 3.8% “Obamacare” tax will apply to all gains on sales of used equipment. Thus, if you fully depreciate an asset, and then sell it in 2014 for $1,000,000, you’re going to pay capital gains tax of at least $238,000 (23.8%) - and perhaps much more after factoring depreciation recapture - with virtually no offsetting tax breaks. Adding to the pain is the fact that your estimated taxes for 2015 will also increase in proportion to the increased taxes you pay in 2014 (you may ultimately be able to claim a deduction or refund, but it will still negatively impact your 2015 cash position).

Maximum impact

This effective “double-tax increase” will, of course, significantly reduce incentives for both rental operators and construction companies/contractors to replace their equipment fleets. Consequently, we expect them to reduce or delay purchases and limit sales of their used equipment to varying degrees in an effort to get another year or two out of those items that might, with some additional care and maintenance, survive and continue to generate revenues, at least until the current tax regime is rationalized and a measure of understanding regarding the importance of tax incentives is reincorporated, perhaps after the next election cycle. In the interim, the obviously negative impact on distributors will continue to be criticized by a wide range of industry participants.

By contrast, the equipment rental market, which is currently expected to grow at a rate of 8.6% annually between 2013 and the end of 2017 (just over 50% in the aggregate during that period), may see greater expansion as a result. The primary question now is whether rental fleets will be large enough to satisfy demand; an uncertainty that appears to be driving renewed interest not only in opening new rental outlets, but also in participating in the “re-rental” or “sub-rental” market (whereby an owner rents equipment to a rental store, which then “re-rents” it to the rental store’s customers). This may create an additional revenue opportunity (perhaps at higher-than-normal rental rates), both for distributors who don’t regularly participate in the equipment rental market and for those seeking to expand their presence in the rental industry without buying or opening completely new rental operations. But as noted below, you will want to make certain you have adequate insurance before proceeding.

What are your legal options?

For those dealers who elect to participate in the rental market, this also highlights some additional legal and financial issues:

- Update Training and Safety Information. Rental operations are likely to see more customers who are unfamiliar with controls, operating characteristics, maintenance requirements and safety information in the coming months. Consequently, most will be well-advised to carefully review and update their familiarization and training processes and make absolutely certain that all manufacturers’ operating and safety manuals are included with, in or on each piece of equipment that goes out on rent (attaching plastic sleeves containing all of the relevant printed materials seems to work well for many).

- Revise Your Rental Contract. Because maintaining your equipment becomes more important as it ages, rental operators need to ensure their rental contracts cover at least the following:?

a) Maintenance: Make customers responsible for protecting and maintaining rented equipment while out on rent;

b) Overuse and Abuse: Require customers to refrain from overusing rented equipment (double- and triple-shifting being common in some areas);

c) Malfunctions/Defects: Require customers to immediately cease using rented equipment that malfunctions, and notify you at the first opportunity (which also helps rental operators determine when an item should go “off-rent”);

d) Use, Care and Safety Instructions: Include acknowledgements by customers of their receipt of, and agreement to comply with, all use, safety, care and maintenance instructions; and

e) Indemnity and Hold Harmless: Make customers liable (indemnify and release claims against you) for mishaps that occur in connection with any compliance failures. Doing so not only helps reduce equipment damage, wear and tear, it also limits the potential for personal injury and third-party property damage claims. - Consider Re-Rentals. As an alternative to allowing equipment to sit idle, more owners are opting to rent it to rental stores for “re-rental” to their customers. Doing so in a high-demand market can be a lucrative proposition, but you will need to make certain you include provisions in your rental contract that adequately address the liability and insurance issues for both your operation and the equipment owner’s (absent which, you may find yourself being squeezed between lawyers for the rental store and the rental store’s customer).

- Consider Creating, a Separate LLC for Rental Operations. Trying to run a rental operation in tandem with a sales operation under the same entity structure is a dubious proposition from both accounting and legal perspectives (think “dual-use” issues and liability exposure for all of your assets). These and other issues weigh in favor of housing your rental operation in a separate company. S-corporations, once the darlings of the corporate world because of the combination of “pass-through” tax status and limited liability they offered shareholders, have become less attractive by comparison to limited liability companies (“LLCs”) which offer similar liability protection and pass-through tax status, but are:?

a) Easier to manage: (for example, they typically don’t require minutes in most cases and generally require much less in terms of “corporate formalities”);?

b) More flexible: (they can be taxed as S-corporations, C-corporations or partnerships; they allow for distributions regardless of percentage ownership, and they can be owned by any number of “members” or “economic interest-holders”); and?

c) Less risky (because they don’t suffer from the ever-present threat of “surrendering your S-election,” the negative tax consequences of which can be substantial, and because an ownership interest in an LLC is generally less attractive to plaintiffs’ lawyers and creditors, whose right of execution is limited, in most jurisdictions, to the “economic interest” in an LLC ownership stake (distribution rights), as opposed to a shareholder’s entire “stock” ownership in an equivalent S-corporation).

Conversion from an S-corporation to an LLC is relatively easy to accomplish, requiring only completion of “Articles of Conversion” (or a similarly named document) and filing them with your Secretary of State in most cases (setting up a new one for a rental operation is also relatively uncomplicated). The filing fee is usually only a few hundred dollars, but once you’ve converted, it may be impossible to reverse. So, I recommend checking with both your accountant and your attorney before proceeding.

The shifting tax environment continues to create new challenges (and opportunities) for distributors and rental operators. As is so often the case, however, this is yet another instance where good planning and preparation can create a significant competitive advantage for those who are properly prepared.

James R. Waite, Esq., is a corporate and commercial equipment leasing attorney with over 20 years of experience. He authored the American Rental Association’s book on rental contracts and is the owner of EquipmentRentalContracts.com. He has represented dozens of equipment rental companies throughout North America. He is also a veteran of the United States Air Force, has a BBA in Finance from the University of Texas at San Antonio, a Juris Doctor from St. Mary’s University, and an MBA from the Kellogg School of Management at Northwestern University in Evanston, IL. He can be reached at (866) 582-2586, or via email at: [email protected].