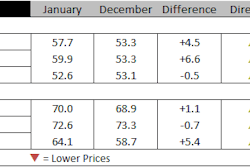

Construction costs rose in March on strength in both materials and labor markets, according to IHS Markit and the Procurement Executives Group (PEG). The headline IHS Markit PEG Engineering and Construction Cost Index registered the fifth consecutive month of rising prices, though the 53.9 reading in March was down from 55.2 in February.

The materials/equipment price index came in at 55.4, below the 58.0 in February. Eight of the 12 categories tracked in the materials sub-index showed rising prices. Ready-mix concrete, turbines and the ocean freight indexes registered flat pricing. No category had falling prices. Transformers and electrical equipment had the largest index figure increase compared to February; index figures rose approximately 10 points for each, illustrating the pass-through from recent raw material price increases.

“Rising input costs are putting upward pressure on transformer pricing. Items like copper and ferro silicon have seen large gains over the past year and this is being passed through to downstream products like transformers,” said Brandon Ruschak senior economist at IHS Markit.

The subcontractor labor index rose in March to 50.3 after dipping below the neutral point in February. Regionally, U.S. Northeast and Midwest had rising labor costs, while in U.S. South and U.S. West, labor costs remained the same compared to February. Labor costs continued to fall in both Eastern and Western Canada.

The six-month headline expectations index recorded another month of increasing prices. The index moved down slightly from 67.5 in February to 67.2 this month. The materials/equipment index stayed positive at 70.6, marginally lower than the 71.3 recorded in February. Despite the slight give-back, this figure affirms widespread expectations of higher future prices. Every component showed rising prices. Sub-contractor labor price expectations came in at 59.3 in March, slightly higher than the 58.6 recorded in February. Labor costs are expected rise in all regions of the United States. They are expected to remain unchanged in Eastern Canada and rising Western Canada.

In the survey comments, respondents have noted shortages for regional sourcing of aggregates as well as for some subcontractor labor categories. Participants continue to express cautious optimism for 2017 and proposal activity index has been up for more than 6 months.

To learn more about the new IHS Markit PEG Engineering and Construction Cost Index or to obtain the latest published insight, please click here.