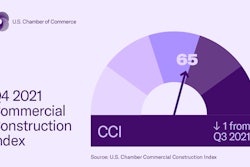

Labor shortages and rising material prices put a drag on the construction recovery during Q3 2021, showed the Third Quarter 2021 Marcum Commercial Construction Index, with nonresidential construction spending still well behind pre-pandemic levels. Nonresidential remains down 1.3% from Q3 2020 and 10.7% below January 2020.

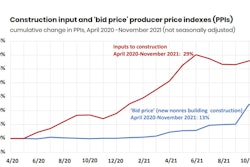

While a softening in the U.S. economic recovery has impacted construction activity post-pandemic, a 19% hike in construction materials prices and the notable decline in the U.S. workforce – which drove up construction labor costs – have proven to be far bigger factors in slowing construction project growth and the industry's recovery, the Index indicated.

Higher Costs and Uneven Job Gains

According to Anirban Basu, Marcum’s chief construction economist and author of the report, inflation and supply chain disruptions have proven to be concerns for both the construction industry and broader economy. One of the factors he cited as driving input prices higher is transportation costs. In addition to dramatic increases in ocean freight costs, domestic transportation costs have surged due largely to a lack of available truck drivers.

“During a recent 12-month period, the cost of truck transportation rose 14%,” Dr. Basu noted.

And while construction job growth has improved, gains have been largely limited to specific industry segments, with residential construction seeing the largest increase. “Residential construction employment has outpaced nonresidential job growth since the start of the pandemic. Of the 169,000 jobs the construction industry has added since October 2020, the residential sector accounted for 122,800 (72.6%) of them,” said Dr. Basu.

“The nonresidential construction segment added 33,000 net new jobs in October 2021 and supports 46,500 more jobs than it did in October 2020,” he continued. “But a majority of that growth has occurred in the heavy and civil engineering sub-segment, which is largely fueled by public financing. Nonresidential building employment, which is largely supported by private investment, is up only 4,700 positions over the past year.”

Ongoing Challenges Impact Profit Potential

With passage of the infrastructure bill and a still-hot residential market, Dr. Basu is optimistic about the construction industry in 2022. However, he warns that current conditions could suppress contractor profit margins.

“Most contractors remain very busy. Demand for construction services remains high,” said Dr. Basu. “The primary issues relate to rising costs, materials shortages and worker shortages. Thus, while the average contractor expects sales and employment to rise over the next six months, profit margins are expected to decline.”

In order to preserve margins, contractors will be required to plan ahead for further cost increases. “Prices are continuing to rise for materials, and the labor shortage is causing timing issues as well as increased overall costs to employ people,” noted Joseph Natarelli, Marcum’s national construction leader. “We strongly urge contractors to lock in material purchases for future projects further out than they normally would in an effort to curb delays as much as possible. It is also important to account for these increased costs in future bids in order to limit further gross profit deterioration.”

Information provided by Marcum LLP and edited by Becky Schultz.