The fourth quarter of 2021 saw the construction industry continue to struggle amidst rising costs and labor and materials shortages, according to the Marcum Commercial Construction Index. Even as expectations improved with respect to business and financial conditions, nonresidential construction activity continued to slide at year’s end.

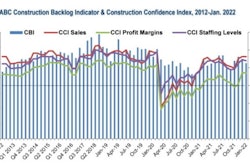

According to the Associated Builders and Contractors’ Construction Confidence Index, more than 65% of contractors expect their sales to increase during the first half of 2022, and the Construction Financial Management Association’s Confindex Indicator suggest that contractors’ confidence is well above year-ago levels, the index notes. Yet, there are challenges that continue to weigh heavily on the market.

“There are certainly many indicators pointing to ongoing construction recovery, including residential building permits and the Architecture Billings Index. The principal challenge will be the labor market conditions, financial conditions, current confidence, and year ahead outlook,” said Dr. Anirban Basu, chief construction economist at Marcum LLP. Marcum’s National Construction Services group produces the index.

Jobs Lag as Inflation Risk Grows

Even as the overall U.S. economy has significant job growth, the construction industry has failed to keep pace in recent months. In fact, it lost nearly 5,000 net jobs in January, with the nonresidential sector seeing a decline of 9,000 jobs, which was only partially offset by a 4,400 job gain in residential.

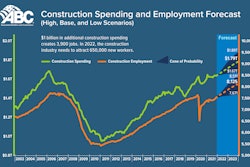

The nonresidential sector has also lagged in overall spending in recent months. While up 3.9% year-over-year, nonresidential saw a further decline of 0.7% in December 2021, the most recent month for which data are available. And with inflation is factored in, year-over-year spending sits below 2020 levels in real terms, despite many projects already in various stages of design.

One likely explanation that this has not translated into rapid nonresidential construction spending growth is high materials costs and the lack of labor, both of which appear to be inducing some project owners to take a wait-and-see approach, Dr. Basu points out in the report. Materials costs remain a significant headwind, but he expects inflationary pressures to subside somewhat by the end of 2022.

“Construction input prices are up 23.5% over the past year, continuing a staggering inflationary run that has characterized much of the pandemic. Certain commodities have experienced particularly sharp increases. Iron and steel prices, for instance, are up more than 105% over the past year,” he commented. However, this should gradually ease. “The expectation is that commodity and materials price increases will become more moderate during the years to come.”

Use Caution Ahead

Despite the challenges, Joseph Natarelli, Marcum’s national construction leader, sees opportunity ahead coupled with the ongoing uncertainty the industry faces. He encourages a cautious approach forward.

“We remain wary of persistent problems surrounding labor challenges, supply chain interruptions and inflation. Inflation for construction inputs is far outpacing the already-high inflation levels in the rest of the economy, so careful pricing and procurement will be vital in the coming year,” he advised. “We also think that most of the industry will need to be mindful of finding and retaining talent as wages climb and demand rises.

“Meeting those challenges while capturing the many growth opportunities will be critical to overcoming these headwinds and thriving in 2022,” he added.

Information provided by Marcum LLP and edited/enhanced by Becky Schultz.