In the end, real estate is all about money. Builders need money to buy land and dig foundations. Buyers need it for down payments and to demonstrate that they can pay their mortgages, taxes, and related costs every month without fail.

These days, the results of trying to build or buy houses without money are all around us - a landscape of builders in bankruptcy and homeowners in foreclosure.

In the fourth year of a struggling housing market and with industry confidence at a very low ebb, builders have gotten the picture - at least from what was said at the recent International Builders Show in Orlando, Fla. Reports of the event's meetings indicate that builders were being urged to focus on affordability.

Affordability is key to the growth of "green" building, for example, with builders maintaining that price is more important to buyers than cutting-edge technology.

One builder has had to find ways to cut costs in other facets of its operation to pay for the products, materials, and quality-control time needed to erect more energy-efficient homes. Together, those things add 3 percent to 5 percent to the costs of construction.

"The problem is that [buyers in] a lot of markets aren't willing to pay for them, so we are taking on the additional costs," the builder, Nate Beauregard of David Weekly Homes in Texas, said at a discussion of green building.

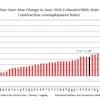

Builders' access to the credit they need to start new homes "remains the fragile component of industry predictions," said David Crowe, chief economist for the National Association of Home Builders, the show's sponsor.

So far, small builders have experienced extreme difficulty in obtaining financing. (Rectifying that situation as soon as possible is the association's top priority.)

It's especially true for multifamily construction. As job creation is beginning to increase the number of people looking for apartments, the dearth of financing is contributing to rent increases now and the likelihood of an apartment shortage down the road.

Multifamily is poised to profit from a disproportionate number of Generation Y members moving into the housing market and has seen the bottom of the cycle, Crowe said. The sector will see starts rise 16 percent this year to 133,000 units, he said, with a further 53 percent increase in 2012 to 203,000 units.

But 133,000 "is far short of the 250,000 to 300,000 units that would be required to keep supply and demand in balance," he said.

In addition, Crowe said, "we have yet to make up for the insufficient number of new apartments that should have been built over the last two years. The capital needed to finance that construction is just not available to apartment developers."

Even affordable rental housing is feeling the pressure.

Robert Greer is president of Michaels Development Co. in Marlton, which builds and manages rental communities here and elsewhere. In Orlando, Greer told builders that although affordable housing, which is driven by the low-income housing-tax credit, appears to be rebounding and investors are returning to the market, "given the depth of the current recession, more people than ever need affordable housing, and the demand far outstrips the supply."

Starts for single-family homes this year will likely total 575,000, a 21 percent climb over 2010's 475,000 units, which was 7 percent more than the 442,000 homes started in 2009, Crowe said.

A 20 percent increase in housing production in 2011 is good news for the industry. But to put things in perspective, Freddie Mac chief economist Frank Nothaft noted that this is a gain from an extremely low level - single-family production declined about 80 percent from peak to trough.

Inquirer real estate writer Alan J. Heavens is the author of "Remodeling on the Money" (Kaplan Publishing). His home improvement column appears Fridays in Home & Design.

![Fod No Caption 74 A Tc M Cy Uy[1]](https://img.forconstructionpros.com/mindful/acbm/workspaces/default/uploads/2026/08/fod-no-caption74atcmcyuy1.vcSFiPTy0m.png?auto=format%2Ccompress&fit=crop&h=100&q=70&w=100)

![Fod No Caption 74 A Tc M Cy Uy[1]](https://img.forconstructionpros.com/mindful/acbm/workspaces/default/uploads/2026/08/fod-no-caption74atcmcyuy1.vcSFiPTy0m.png?ar=16%3A9&auto=format%2Ccompress&dpr=2&fit=crop&h=135&q=70&w=240)