Low financial stress, an expanding housing sector, and increased federal spending on infrastructure are expected to propel equipment and software investment growth of 4.6% for 2022. Annual U.S. GDP growth for 2022 is forecast at 3.5%, according to the 2022 Equipment Leasing & Finance U.S. Economic Outlook released by the Equipment Leasing & Finance Foundation.

The Foundation’s report, which is focused on the nearly $1 trillion equipment leasing and finance industry, highlights key trends in equipment investment and places them in the context of the broader U.S. economic climate, providing the U.S. macroeconomic outlook, credit market conditions and key economic indicators.. It is produced n partnership with economic and public policy consulting firm Keybridge Research and will be updated quarterly throughout 2022.

Nancy Pistorio, Foundation Chair and President of Madison Capital LLC, said, “This report provides a thorough examination of the wide range of conditions that will impact the U.S. economy and business investment next year. Despite uncertainty around new Covid variants, ongoing supply chain issues and inflation, positive factors should outweigh the headwinds. Robust consumer demand, a strong labor market, and increased equipment and software investment — the lifeblood of the equipment finance industry - -look promising. We can look forward to ‘getting back to business’ in 2022, provided supply chain issues ease significantly and the pandemic is effectively curbed.”

Highlights from the 2022 Outlook

While equipment and software investment is forecast to grow 4.6% (annualized) in 2022, supply chain constraints, high inflation and tighter monetary policy are key headwinds to growth. The U.S. economy slowed in fall 2021 as the pandemic worsened and supply chain constraints snarled global trade and drove inflation to multi-decade highs. However, growth in Q4 has likely rebounded, and the economy appears poised for an above-average year in 2022.

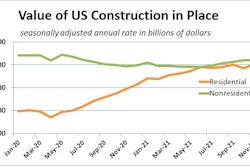

The U.S. manufacturing sector should continue to expand at a healthy rate in 2022, although supply chain issues, hiring difficulties and high inflation could dampen industrial sector output, particularly during the first half of the year.

On Main Street, the outlook has grown increasingly cloudy. Small firms are more susceptible to surging input costs and labor scarcity than large firms, which may weigh on small businesses as the new year gets underway. On the positive side, consumer demand remains robust and the winter months should be smoother this year than last.

Federal Reserve officials recently shifted their positions in response to new data and now acknowledge that inflationary pressures are likely here to stay. The Fed is expected to end quantitative easing earlier than planned and raise interest rates at least once by mid-2022. Multiple rate hikes are possible in 2022, particularly if job growth stays on track.

Investment Momentum Outlook

The Foundation-Keybridge U.S. Equipment & Software Investment Momentum Monitor, which is released in conjunction with the Economic Outlook, tracks 12 equipment and software investment verticals. In addition, the Momentum Monitor Sector Matrix provides a customized data visualization of current values of each of the 12 verticals based on recent momentum and historical strength.

Eleven verticals are peaking/slowing, and one is accelerating. Of those relevant to the construction industry and heavy equipment sector, over the next three to six months, year over year:

- Construction machinery investment growth will decelerate, though likely remain in positive territory.

- Materials handling equipment investment growth should remain positive.

- Agriculture machinery investment growth will continue to decelerate.

- All other industrial equipment investment growth should slow.

- Mining and oilfield machinery investment growth should stay strong.

Relative to the supply chain, which in 2021 proved a major factor in construction materials costs and project completion, over the next three to six months, year over year:

- Trucks investment growth should remain healthy.

- Aircraft investment growth will continue to decelerate, though remain positive.

- Ships and boats investment growth is expected to remain in healthy territory.

- Railroad equipment investment growth is expected to remain strong.

In addition, the report shows computers investment growth should remain positive, but is unlikely to accelerate, while software investment growth may have peaked, though should remain robust.