As much as we all want to put 2021 in the rearview mirror, the supply chain and labor issues initiated by the COVID-19 pandemic are expected to persist into 2022.

Many manufacturers were hoping supply chain disruptions would start winding down by now, but we are facing sourcing issues well into this year, and when things will get back to normal is really a guessing game at this point. So, while the recently passed infrastructure package should help generate new construction activity, sourcing materials and equipment may prove challenging, at least in the first half of the year.

In terms of labor, Gen X, which has been the bedrock of the skilled labor workforce, retired in record numbers during the pandemic. The industry has not developed a talent base to replace those who have left, which will prove to be an ongoing challenge. Technology is one answer to help in the short term, but the industry needs to attract a new generation of workers while competing with almost every other industry that has found itself facing shortfalls, as well.

To get a gauge on these and other factors likely to impact construction in 2022, we reached out to several leading industry economists to get their outlook on both the headwinds and opportunities the industry is facing.

Q: What are likely to be the major drivers of the commercial and housing construction markets in 2022 and do you anticipate the current level of new construction to be sustained in both segments?

Ken Simonson, chief economist, Associated General Contractors of America (AGC)

Ken Simonson, chief economist, Associated General Contractors of America (AGC)

The most widespread positive expectations were for infrastructure categories — highway and bridge, transportation facilities and water and sewer projects — which most likely reflects optimism about funding boosts from the recently enacted Infrastructure Investment and Jobs Act (IIJA). But there were also strongly positive net readings (that is, the percentage of respondents who expect the dollar value of projects to increase minus the percentage who expect a decrease) for such predominantly private sector categories as warehouses, hospitals and other healthcare, which includes clinics, testing facilities and medical labs. The only negative views, on net, were for retail and private office construction.

Richard Branch, chief economist, Dodge Construction Network (Dodge)

Richard Branch, chief economist, Dodge Construction Network (Dodge)

Construction starts should show notable improvement in 2022, fed by the strengthening economy, the numerous projects in the planning pipeline and the recently enacted infrastructure program. This optimism, however, will be countered by continued high material prices, shortages of key materials and an acute shortage of skilled labor.

For 2022, we anticipate that total construction starts will post 9% growth over 2021. While residential construction will continue to play a large role in [this year’s] growth, a more balanced recovery in the nonresidential sector will begin.

Anirban Basu, chief economist, Associated Builders and Contractors (ABC)

Anirban Basu, chief economist, Associated Builders and Contractors (ABC)

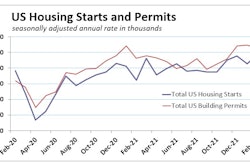

The demographics of America are quite conducive to home sales as millennials come of age. The biggest thing here is the inventory of unsold homes continues to be very low. That represents an opportunity for builders to meet unmet demand. Based on recent housing starts data, that’s precisely what they are doing.

It is conceivable that at some point there will be a bit of a housing supply bubble. It’s not happening now. Most neighborhoods are associated with a dearth of available inventory. There isn’t enough housing to purchase. We are seeing that private equity is getting involved. They’re beginning to build more houses and renting them out. At some point, those houses will hit the market for sale and, at that point, we may see some excess supply in certain communities. But for right now, the market for housing supply is very strong, and that’s both single-family and multifamily.

Danushka Nannayakkara-Skillington, assistant vice president for forecasting and analysis, National Association of Home Builders (NAHB)

Danushka Nannayakkara-Skillington, assistant vice president for forecasting and analysis, National Association of Home Builders (NAHB)

On the supply side, we have a housing deficit right now. Freddie Mac estimates it to be 3.8 million units, and the National Association of Realtors is estimating the housing deficit to be above 5 million. At NAHB, we estimate around a 1 million deficit. The combination of these factors are driving residential construction right now — the demographics tailwind and the housing deficit.

We are forecasting single-family construction to be flat (up only 1% growth compared to 2021) in 2022. This is because of the supply side issues, which are not just high cost of building materials but the lack of skilled labor, lack of buildable lots, access to AD&C financing and high regulatory costs. All of these issues together are hampering single-family construction. For the multifamily housing segment, we are forecasting strong growth, up 6% compared to last year. We anticipate close to half a million multifamily units for 2022.

Q: What are likely to be the major drivers for public construction in 2022 and do you anticipate the current level of new construction to be sustained? In which subsets do you expect to see the greatest uptick or downturn in activity?

AGC: States and many local governments are generally in good fiscal shape and should be able to devote more funds to infrastructure, thanks in part to federal dollars received over the past two years.

In addition, federal funds from the IIJA, also known as the bipartisan infrastructure bill, will begin to be awarded in 2022, although actual construction will ramp up more slowly. Highway and bridge projects are likely to get started the soonest, but the largest percentage increases are likely to go over time to water, sewer, broadband and alternative energy projects that have not previously received much federal funding. The multi-year legislation should assure funds continue flowing for several years.

AGC of America’s annual Hiring and Business Outlook Survey, which drew more than 1,000 responses from contractors in every state, found respondents expect bidding opportunities to increase in 15 out of 17 market segments.

AGC of America’s annual Hiring and Business Outlook Survey, which drew more than 1,000 responses from contractors in every state, found respondents expect bidding opportunities to increase in 15 out of 17 market segments.

Office space demand obviously is down thanks to remote working. Occupancy rates look pretty reasonable in many cases, but they are a false read. In many cases, buildings are legally occupied because there’s a lease involved and the property was leased before the pandemic. In fact, many of these office buildings are largely empty. Very few workers have returned to date. The omicron variant will merely extend that period. As office space leases come up for renewal, you will see many office space users end up leasing less space or perhaps no space at all.

Finally, hotels that cater to business travel will continue to suffer from less than the typical occupancy for obvious reasons as business is conducted by Zoom and Go To webinars. There has been some recovery, but if one is looking for complete recovery, that probably proves elusive for quite some time.

These changes could be somewhat permanent. Once Americans get accustomed to doing things a certain way, that remains in place. A recent survey indicated 68% of Americans prefer to work from home or remotely. That’s going to have an effect on the office market into the very long term.

Dodge: It will be a challenge for the construction sector to maintain the 2021 level of activity in 2022. However, as the recovery in construction evens out, there will be more opportunity spread across numerous project types in both the public and private space, including:

- Warehouses/Fulfillment centers

- Multifamily

- Data centers

- Manufacturing

- Healthcare

- Education

Q: What factors could play an instrumental role in raw material costs in 2022? How will the ongoing supply chain shortages impact the costs of raw materials or other construction inputs?

AGC: Fortunately, materials costs are no longer rising across the board. For instance, Steel Market Update’s hot-rolled coil price tumbled more than 20% from early September to early January. But the price was still nearly triple the pre-pandemic level of early 2020. Thus, prices may not set new record highs in 2022, but they are likely to remain volatile and unlikely to sink back to earlier marks.

The supply chain remains fouled up with very unpredictable production and delivery times. Supplies are still very vulnerable to events such as the freeze last February in Texas that knocked out production of resins for a host of construction plastics.

ABC: During the first half of 2022, contractors continue to expect raw material prices to remain elevated. The global supply chain disruptions remain in place. America just passed an infrastructure package, which of course will actually increase demand for certain materials — steel, for instance.

With most construction segments expecting positive growth, labor and materials will be the biggest challenges in 2022.

With most construction segments expecting positive growth, labor and materials will be the biggest challenges in 2022.

It is conceivable at some point, perhaps through the latter stages of next year, that you could see the bottom fall out of some of these commodity prices. What might happen is that demand growth begins to stall because we have come out of the pandemic. Demand stabilizes instead of ratcheting higher as we reopen the economy. Meanwhile, suppliers have had a lot of incentive to increase capacity because the price is right and that’s a profit-making opportunity. All of that can come together... to conspire to cause prices to dip, but as we enter 2022, it appears that we are poised for quite high prices.

Many contractors have lost some degree of work because bids have come in too high. There is nothing they can do about it. The materials cost what they cost and the workers cost what they cost. But that’s an issue for the industry.

Many construction financial professionals are somewhat downbeat about 2022. There’s lots of design work taking place. The backlog is reasonably healthy in many cases. But they realize they have a problem. They must deliver these contracted services while still maintaining margins. Many are concerned they are not going to be able to maintain profit margins at the current level in 2022.

Dodge: Rising costs, skilled labor shortages and lack of materials continue to create challenges for general contractors and their clients, sending the U.S. Chamber of Commerce Commercial Construction Index down one point to 65 in the final quarter of 2021. Revenue expectations, a key driver of the overall score, fell among Index survey respondents for the first time since the start of the pandemic to 58, down three points from Q3 of 2021.

There is, however, reason to believe that we’re starting to see the very faint glimmer of the light at the end of the tunnel. Factory output in the U.S. is broadly back to where it was prior to the pandemic, and the most recent reading of the Purchasing Managers Index suggested that supplier delivery times were speeding up, albeit slowly. This suggests that by mid-year, price inflation should begin to ease somewhat and provide relief for builders.

An uncertain element, though, is how APAC nations will respond to the omicron and future [coronavirus] variants. Some Asian countries have been more strict in enacting lockdowns in response to the growing number of cases. So, while domestic production should improve and provide relief, firms that rely on overseas components may continue to struggle in sourcing materials.

NAHB: Over the past four months, lumber prices have nearly tripled, causing the price of an average new single-family home to increase by more than $18,600. This lumber price hike has also added nearly $7,300 to the market value of the average new multifamily home, which translates into households paying $67 a month more to rent a new apartment. NAHB calculated these average home price increases based on the softwood lumber that goes into the average new home, as captured in the Builder Practices Survey conducted by Home Innovation Research Labs.

The framing lumber prices at the peak were adding $30,000 to the price of a single-family house and $10,000 to a multifamily house. The price increases were due to a shortage induced by the COVID pandemic. Mills curtailed production in anticipation of slower demand in April of 2020. While the demand held up better than predicted, the mills did not immediately ramp up production, which has led to the current pricing.

Aluminum and copper prices are stable right now, but they are at historical levels right now, too. China is the largest producer of raw aluminum and it has been shutting down aluminum manufacturing around the country since 2020 to cut greenhouse gas emissions. This is the primary reason for the price increases in aluminum.

Q: How has the nationwide labor shortage affected the construction industry? What are your projections for the labor market in 2022, particularly when it comes to skilled trades?

AGC: One sign of improving conditions in nonresidential construction is that the sector added jobs for each of the last four months of 2021, following five straight months of decreases. The gains should continue.

Three-fourths of the respondents to the AGC Hiring and Business Outlook survey said they expect their firms will add workers in 2022. But it won’t be easy. An overwhelming 83% reported having a hard time filling some or all salaried or hourly craft positions. That’s not surprising, given that the unemployment rate among former construction workers was only 5.0% in December, tying the lowest December rate since the series began in 2000.

Meanwhile, there were 345,000 job openings in construction at the end of November, a 32% leap from a year earlier and the highest November total in the 21-year history of that series. These data all point to a tough year for firms looking to add trades workers.

Dodge: A Dodge study found that in Q2 of 2021, the volume of work for civil contractors increased; 40% of contractors reported an increase in their backlogs compared to just 25% in Q1 2021. Beyond an increase in work and increasingly complex supply chain issues, there is a new shortage complicating construction: skilled labor. According to a Dodge survey of contractors, 60% reported a high need for skilled workers.

We have reason to believe that this trend will continue into 2022. With a high need for labor and a small pool of laborers, many contractors believe it will be a big haul to find skilled workers, thus stretching the timeline to complete projects and meet schedule requirements.

NAHB: We estimate that we need more than 61,000 new hires every month in construction to keep up with the industry growth and the loss of workers to retirement. This will require an additional 2.2 million new hires for construction from 2022 to 2024. That’s a staggering number of workers that we need as an industry. Right now, for residential and nonresidential, the average job openings rate is around 300,000 or 400,000 positions each month.

We need more young people to come into the trades. We need to reach out to secondary school students and talk to parents and talk to teachers and change their perspectives on careers in construction.

ABC: In some sense, these labor shortages are nothing new. The industry was wrestling with them prior to the pandemic and has been talking about them for years. What happened during the pandemic which was new was that so many baby boomers retired early — about 1.5 million retired earlier than they had anticipated for various reasons. Many of them were the best construction workers. They wanted to work with equipment; that was their dream. Not as many young people have construction as their dream, but these baby boomers often did.

None of the young people have exposure to the trades. Not many of them understand that this is a pathway to American prosperity, a pathway to the middle class, a pathway to entrepreneurship.

America’s labor force is, frankly, too small right now. We’ve had precious little immigration in recent years and birth rates are much lower than they used to be. As legal immigration has slowed, we just do not have enough labor force participating in construction. You put all that together and there are not enough workers out there. This affects certain segments more than others, including construction, because we don’t have enough carpenters, glazers, roofers, electricians, plumbers and pipe fitters.

What that means is labor costs will continue to rise in 2022. That is divorced from the supply chain issue. You can solve the supply chain issue and you will still have a shortage of carpenters in this country.

Summing it up

Despite the challenges of sourcing labor, materials and equipment, 2022 promises to offer more opportunities for growth. If you discount retail and office space construction, most other construction segments promise expansion through 2022.

The trick is going to be planning ahead and positioning your company to take advantage of the opportunities in the face of critical shortages.