Midyear update of the Dodge Construction Outlook raises expectations for total U.S. construction starts to a 2012 increase of 2%, to $445 billion. While slightly better than flat 2012 performance predicted last October, the updated forecast still portrays an industry struggling for upward momentum.

"The construction industry has yet to move from a hesitant up-and-down pattern to more sustained expansion

"After plunging 23% in 2009, new construction starts edged up only 1% in 2010 and were unchanged in 2011, so the modest 2% increase predicted for 2012 is really more of the same," stated Robert A. Murray, vice president of economic affairs for McGraw-Hill Construction. "The backdrop for the construction industry remains the fragile U.S. economy, which continues to see slow employment growth, diminished funding from federal and state governments, and the uncertainty related to the U.S. fiscal stalemate and the European debt crisis. On the plus side, energy costs are now receding, interest rates are very low, and lending standards are beginning to ease for commercial real estate development."

The construction market this year continues to see a mix of pluses and minuses by major sector:

- Single family housing will advance 21% in dollars on a 19% increase in the number of units to 490,000. While still at a very low level, single family housing has registered small, steady gains over the year.

- Multifamily housing will climb 19% in dollars and 18% in units. Rising occupancies and rents reflect elevated demand from potential homebuyers reluctant or unable to purchase single family homes.

- Commercial building will grow 10% following the 12% 2011 gain. Warehouses and hotels will see the largest increases, joined this year by a moderate gain for stores. Office construction will see more privately financed projects but less government spending.

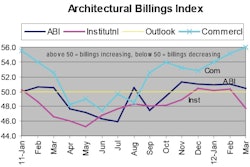

- Institutional building construction will fall 10% after sliding 11% in 2011. The tough fiscal environment for states and localities continues to dampen school construction, and uncertainty in the general economy is restraining healthcare facilities.

- Manufacturing construction will retreat 20% following the 75% jump in 2011, which featured the start of several unusually large projects.

- Public works construction will slide an additional 6% after last year's 14% decline, reflecting government spending cuts and the absence of a multiyear federal transportation bill.

- Electric utility construction will hold steady with its exceptionally strong 2011 amount, helped by this year's start of two large nuclear power projects.

Copies of the report will be available on June 28th at http://analyticsstore.construction.com/index.php.

Additional reports and projections are available from McGraw-Hill Construction Research and Analytics, http://construction.com/market_research.