Business is so good, we are placing concrete every day. To maximize revenue and service to customers, we need concrete placement equipment on demand. Our local pumper is top-notch; he almost always finds a way to get our work done. But, we are not the only busy concrete contractor and it is reasonable to expect that his schedule will impact our schedule at some point this season. My accountant thinks we are paying too much rental, and that we could use some depreciation? Are we paying enough pump rental fees to justify purchasing our own pump?

Reasons to rent pumps

- You have access to the pumper’s fleet when you need more than one.

- You have no maintenance costs.

- You can rent the right boom length for the job.

- Rental fees are deductible so it reduces your taxable income.

Reasons to own

- Control your schedule

- A new pump is a like a billboard for your business that advertises your commitment.

- Capitalize on the profits of pumping concrete.

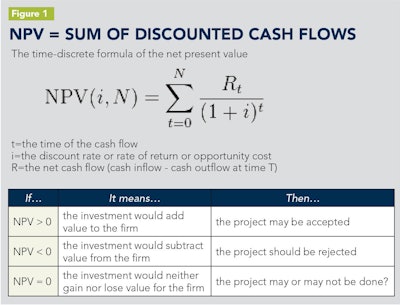

Total Cost of Ownership and Net Present Value are standard financial tools used to analyze these types of decisions. The TCO gives you a more complete picture of the costs involved in owning the equipment and is helpful in comparing similar alternatives. The NPV helps you predict whether or not a particular decision results in a positive net present value. Net Present Value (NPV) is defined as the sum of the present values (PVs) of individual cash flows related to a project or decision. NPV is a central tool in discounted cash flow analysis and is a standard method of using the time value of money to appraise long term projects or decisions. (See Figure 1)

Total Cost of Ownership

Total Cost of Ownership is a philosophy, methodology, or tool for analyzing all of the relevant quantitative and qualitative costs of an acquisition, project, investment, or relationship for the purpose of making a decision.

- Looks beyond/deeper than just the purchase price.

- Seeks to understand value of competitive sales claims.

- Considers ‘value’ of partner relationships.

- Includes relevant information that is often ignored such as residual value or resale value.

For this situation we will define Total Cost of Ownership as:

TCO = (A – R) + O – DTV

TCO = (Acquisition minus Residual Value) plus Operating Costs minus Depreciation Tax Value.

Acquisition minus residual equals machine sales price plus interest minus the residual value at the end of the evaluation period, whether five or ten years.

Operating costs equals fuel, oil, grease, pipeline, wear parts, repair parts, operator wages, mechanics wages, insurance, licensing.

Depreciation value equals tax value of depreciation using five years straight line depreciation.

For both the NPV and TCO analysis, it is necessary to make educated assumptions about:

- Decision time frame – usually five or ten years.

- Projected equipment residual values at these intervals.

- Equipment utilization

- The hourly value of the equipment you want to purchase so you can assess revenue generation (inflows).

- Complete operating costs driven by your utilization: — Fuel, oil, grease, pipeline, wear-parts, broken stuff, operator wages, mechanic wages , insurance and license.

With these predictable figures, we are in a position to build a spreadsheet model that will predict TCO and NPV.

The Sales and Utilization worksheet forms the basis for establishing revenue generation and it drives operating costs. (See Figure 2) In this example we are making the assumption we can utilize a 36 Meter pump 17 days per month/11 months per year – averaging 75 cubic yards per day. For revenue we are using the average rate we pay for this size pump in our market.

To begin the TCO analysis we first establish the acquisition cost of the machine we are considering and adjusting for residual value at the conclusion of our five year analysis period. (See Figure 3) We are also showing 10 years. In this example we are buying a new Schwing 36X concrete pump and assuming its five year value will be 55% of new.

The operating costs flow directly from utilization and the cost assumptions made concerning unit costs; fuel, operator, parts, etc. The TCO can be a very good tool for comparing manufacturer specific costs advantages such as fuel consumption, repair parts, repair labor, and resale value. (See Figure 4) It should be noted that this table smooths osts into neat and tidy monthly costs, and that real life has more peaks and valleys. Replacing a boom pipe might be an annual event, or bi-annual, but the costs could be viewed as happening daily, monthly, etc.

Back to your accountant saying you could use depreciation. Inherent with machinery investment is the depreciation expense that comes with it. This expense reduces your taxes and therefore has a value that is predictable, based on your tax rate, depreciation method, and the value of the equipment being depreciated. In this example we’ve use a tax rate of 35 percent and straight line depreciation (in the NPV). It might seem odd that this shows up as an inflow, or cash positive, but keep in mind we have already fully accounted for the acquisition cost of the machinery above. (See Figure 5)

Now that we have a better view of the total cost of ownership, let’s consider whether this is a money-maker by placing our inflows / outflows into a NPV table. The present value interest factor is based on an eight percent discount rate. (See Figure 6)

Conclusion

Based on our assumptions regarding utilization and operating costs we are predicting a very positive NPV of $410,353. This is a very strong indicator that the decision to own this equipment adds value to your firm. There’s no doubt every situation has its own complexities. There are many more facets to the decision and it makes good sense to challenge some of your assumptions and do several versions of the TCO and NPV. Is the utilization figure too high? Are the operator costs in line? Is the rental rate correct?

To summarize the Capital Equipment Cost Justification outlined above:

- Assess expected utilization and the rental value of the machine you are considering.

- Estimate the operating costs using your utilization.

- Consider the unique value claims of the model(s) you are considering. Does one machine hold value better? Are there operational cost advantages? Fuel? Parts? Repairs? Will some features help you improve utilization?

- Talk to your accountant about depreciation and its value in your situation.

- Talk to your sales representative who will be able to help construct comparative TCO’s and NPV’s for your situation.

- Use some form of Total Cost of Ownership worksheet and a Net Present value assessments AND challenge what you come up with, then...

- Invest in the machine that best fits your use profile, but only if the NPV is positive – using your best view of the TCO.

Ed. Note: Tom Oury currently serves as the Central Region Sales Manager for SCHWING America. Oury can be reached at [email protected].