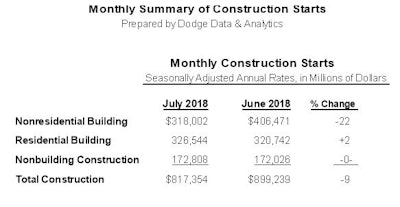

At a seasonally adjusted annual rate of $817.4 billion, new construction starts in July fell 9% from the elevated pace reported in June, according to Dodge Data & Analytics. The latest month’s decline followed strong gains for total construction starts during the previous two months, with May up 14% and June up 11%.

By major sector, nonresidential building dropped 22% after soaring 59% in June, which had been lifted by the start of two massive manufacturing plants and two massive office buildings. While July did see several large manufacturing and office projects reach groundbreaking, they were not the same magnitude as what took place in June. The other two major sectors in July held close to their June amounts, with residential building up 2% and nonbuilding construction unchanged.

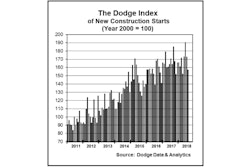

The July statistics produced a reading of 173 for the Dodge Index (2000=100), down from the 190 for June which was the highest level so far during 2018. Looking at the first six months of 2018 on a quarterly basis, which eases some of the swings present in the monthly data, the Dodge Index averaged 165 during the first quarter and 170 during the second quarter. July’s 173 shows that at least the initial month of the third quarter is continuing the gradual upward trend shown by the first two quarters of this year.

“The pattern of construction starts on a monthly basis is often affected by the presence or absence of very large projects, and several exceptionally large projects boosted activity in June to an unsustainably high amount,” stated Robert A. Murray, chief economist for Dodge Data & Analytics. “These June projects included a $6.5 billion uranium processing plant in Tennessee and a $1.7 billion petrochemical plant in Texas, as well as the $1.8 billion Spiral office tower in New York NY and a $665 million office tower in Chicago IL.

"While July also featured the start of several large projects, such as a $2.4 billion petrochemical plant in Texas and a $750 million data center in Alabama, the lift from very large projects in July was less than what took place in June. Still, the pace of construction starts in July came in 2% above the average for the second quarter, which is consistent with the sense that overall construction starts continue to trend upward, notwithstanding July’s steep decline compared to June.

"The current year has seen the mounting headwinds of higher material prices and higher interest rates," he continued, "but it’s also seen the tailwinds of healthy economic growth, some easing of bank lending standards, and the increased funding for public works programs coming from the federal appropriations legislation passed in March. Amidst the monthly ups-and-downs, the broad trend for construction starts during 2018 remains one of modest expansion.”

Nonresidential building in July was $318.0 billion (annual rate), down 22% from June’s heightened volume. The manufacturing plant category plunged 60% from June, which had been boosted in particular by the U.S. Department of Energy’s $6.5 billion uranium processing facility in Oak Ridge TN. If this project is excluded from the June construction start statistics, manufacturing building in July would have shown a 37% gain, while only modest declines would have been reported in July for nonresidential building, down 3%; and total construction, down 1%. July did include the start of a $2.4 billion petrochemical plant in Channelview TX and a $400 million submarine manufacturing facility in North Kingstown RI.

The commercial building categories as a group slipped 5% in July after the 25% increase reported in June. Office building fell 23% from June that included the $1.8 billion Spiral office tower in the Hudson Yards district of Manhattan and a $665 million office tower on North Wacker Drive in Chicago IL. The office building category in July did see groundbreaking for three very large data centers – a $750 million Facebook data center in Huntsville AL, a $600 million Google data center in Stevenson AL, and the $288 million Sentinel data center in Sterling VA. Large office buildings that reached groundbreaking in July were the $250 million office portion of the $330 million Block 71 mixed-use building in Austin TX, a $181 million office building in Chicago IL, and a $97 million Avalon office building in the Atlanta GA area. Through the first seven months of 2018, the top five metropolitan areas ranked by the dollar amount of new office starts were – New York NY, Washington DC, Chicago IL, Omaha NE, and Boston MA. (The Omaha NE metropolitan area included a $1.0 billion Facebook data center expansion that was entered as a May construction start.)

Warehouse construction starts eased back 1% in July, although the latest month featured the start of three Amazon fulfillment centers located in Spokane WA ($181 million), Tulsa OK ($150 million), and Burlington NJ ($150 million). On the plus side for commercial building in July, hotel construction jumped 37% with the help of the $450 million Omni Boston Seaport Hotel in Boston MA, the $212 million hotel portion of the $300 million Aman Hotel & Condominiums in New York NY, and a $150 million JW Marriott Hotel in Tampa FL. Store construction improved 10% in July, and the commercial garage category rose 6% with the help of a $100 million parking deck project at Atlanta’s Hartsfield-Jackson International Airport.

The institutional building categories as a group dropped 10% in July, following a 13% increase in June. The healthcare facilities category pulled back 35% after its 110% June hike, although the latest month did include the start of a $188 million hospital in Los Angeles CA, a $100 million hospital in Easton PA, and a $100 million hospital in Quakertown PA. The amusement and recreational facility category dropped 25% in July, falling for the second month in a row. Educational facility construction retreated 12% after June’s 21% increase, even with the July start of several large high school projects such as a $128 million high school in Saugus MA and a $115 million high school in Roseville CA.

Running counter to the broad decline for institutional building in July was a 28% increase for transportation terminals, led by two noteworthy airport terminal projects – the $650 million main terminal upgrade at Denver International Airport and the $268 million Concourse D project at Nashville International Airport. The public buildings category jumped 56% in July, reflecting groundbreaking for the $207 million Center for Law Enforcement and Public Health in Philadelphia PA, and church construction edged up 2% from a very weak June.

Residential building in July was $326.5 billion (annual rate), advancing 2%. Single family housing registered a modest 3% gain, although in a broad sense this project type continues to hover around the level of activity established at the end of 2017. By geography, single family housing showed this performance for July – the South Central and West, each up 5%; the South Atlantic, up 2%; and the Midwest and Northeast, each unchanged from the previous month.

Multifamily housing in July receded 1%, after the 8% gain reported for June. There were seven multifamily projects with a construction start cost of $100 million or more that reached groundbreaking in July, matching the seven such projects that were reported for June. The large multifamily entries in July were led by the two projects in Brooklyn NY – the $524 million multifamily portion of a $600 million mixed-use building and the $375 million redevelopment of what had previously been a Macy’s garage. Other large multifamily projects that reached groundbreaking in July were a $200 million multifamily tower in Houston TX and the $174 million multifamily portion of a $255 million mixed-use building in Los Angeles CA. In July, the top five metropolitan areas ranked by the dollar amount of multifamily starts were – New York NY, Washington DC, San Francisco CA, Chicago IL, and Los Angeles CA. Metropolitan areas ranked 6 through 10 were – Houston TX, Dallas-Ft. Worth TX, Baltimore MD, Boston MA, and Denver CO.

Nonbuilding construction in July was $172.8 billion (annual rate), holding steady with the pace reported in June. The public works categories as a group were up a slight 1% in July, following a 34% slide in June. Highway and bridge construction grew 8%, helped by such July projects as a $203 million state highway tollway in the McAllen TX area and a $177 million bridge rehabilitation project in Boston MA. Through the first seven months of 2018, the top five states ranked by the dollar amount of highway and bridge construction starts were – California, Texas, Florida, New York, and Pennsylvania.

Sewer construction jumped 70% in July, aided by the start of the $225 million headworks facility in San Francisco CA. The other two environmental public works categories retreated in July, with water supply construction down 1% and river/harbor development down 17%. The miscellaneous public works category (pipelines, mass transit, and site work) fell 29% in July. Offsetting the slight gain reported for public works in July was a 4% decline for electric utilities/gas plants. Providing some support to July’s electric utility/gas plant total were the start of five large wind farms, with three located in Iowa ($450 million, $250 million, and $136 million), while two were located in North Dakota ($225 million and $85 million).

The 2% gain for total construction starts on an unadjusted basis during the January-July period of 2018 reflected a varied pattern by major sector. Residential building year-to-date increased 7%, with single family housing up 7% and multifamily housing up 6%. Nonresidential building year-to-date grew 1%, as a 52% jump for manufacturing plant construction offset slightly weaker activity for commercial building, down 3%; and institutional building, down 5%. Nonbuilding construction year-to-date dropped 4%, with a 52% plunge for electric utilities/gas plants outweighing a 7% rise for public works.

By geography, total construction starts during the first seven months of 2018 revealed this performance – the South Central, up 11%; the South Atlantic, up 6%; the Midwest, unchanged from the same period a year ago, the Northeast, down 3%; and the West, down 4%.