On Dec. 16, the Senate finally approved the Tax Increase Prevention Act (TIPA or H.R. 5771). The bill reinstates dozens of tax provisions that expired at the end of 2013, including 50% bonus depreciation and increased Sec. 179 expensing levels ($500,000 with a $2 million phase-out cap). The White House has indicated President Obama will sign the TIPA. Garry Bartecki, managing member of GB Financial Services LLP and a consultant to the Associated Equipment Distributors, shares his insights on what the announcement means to equipment buyers.

Well, they finally did something useful - Congress, that is. They extended the 50% bonus depreciation and increased the Section 179 to $500,000 with a $2,000,000 equipment purchase cap.

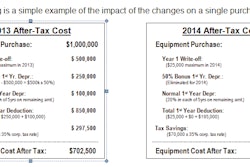

If you purchased equipment and it will have been delivered and “in the dirt” by December 31, 2014, you have the option of using the 50% Bonus for new equipment purchases, or the Section 179 expense write-off up to $500,000 for both new and used equipment, assuming you do not have fixed asset acquisitions exceeding $2 million. After $2 million, the 179 deduction is reduced dollar for dollar; when you hit $2.5 million of asset purchases, Section 179 is no longer available.

The benefit of bonus depreciation is the ability to use it for a carryback or carryforward. Since the bonus may not be available for 2015, it is a good play to use it while you can.

You need taxable income to use the Section 179 deduction. You can’t carry it back, but you can carry it forward and use the then-current rate to reduce taxable income. So if you carry it forward and Congress changes it back to a lower amount, you are stuck with the lower amount until you use it all, and that could take some time at $25,000 per year.

To add to the confusion, please note that if you use the Section 179 deduction, you have to use it before you use the bonus. You can use both or just the bonus. Bonus depreciation gives you about a 60% deduction in year 1, with 179 providing a 100% deduction if you meet the 179 criteria.

Whether you are an OEM, a dealer, a rental company or a contractor, you all have the ability to use both of these extenders. Obviously, larger benefits in terms of a write-off percentage of taxable income will accrue to dealers, rental companies and contractors.

So far, these tax extenders only apply to 2014 because we expect tax reform to get started in 2015. But you still have time to reduce your 2014 tax bill by purchasing a piece of equipment and getting it delivered by December 31, 2014.

For more information about TIPA's bonus depreciation and Sec. 179 provisions please visit depreciationbonus.org, which is maintained by the Associated Equipment Distributors to help equipment distributors and their customers understand these important capital investment incentives.