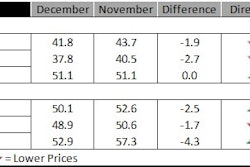

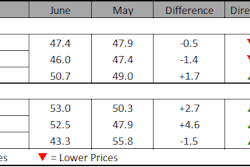

Construction costs fell again in May, according to IHS (NYSE: IHS) and the Procurement Executives Group (PEG). The headline current IHS PEG Engineering and Construction Cost Index (ECCI) registered 47.9 in May, up from April’s reading, but still below the neutral mark. The headline index has not indicated rising costs since December 2014.

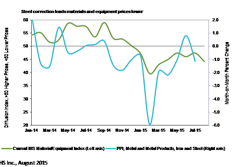

The current materials/equipment index registered 47.4 in May, an improvement from April, but still consistent with the overall narrative of softer prices. Five of 12 individual components registered falling prices this month, with the lowest readings in carbon steel pipe and fabricated structural steel.

“Steel prices are feeling the last of the pull-down from lower input costs; iron ore prices have rebounded over the past few weeks, so this effect will phase out shortly,” said Jason Kaplan, IHS senior manager. “That said, steel plate prices continue to be depressed by a combination of low demand – caused by a drop-off in oil- and gas- related investment – and strong supply, especially from plate being imported from Asia. This is also depressing prices of steel pipes rolled from steel plate. The weakness in the plate market will continue until supply is adjusted in the light of demand.”

Six components did show higher prices in the materials/equipment index in May, led by ready-mix concrete. Additionally, copper-based wire and cable showed higher month on month prices for the first time since September. This comes after it registered the softest reading of any component in February and March and follows the recent gains in copper prices this month.

“The recent push in copper prices to around $6,400/mt is linked to the dollar’s recent retreat and short covering. We do not believe this rally can be sustained on fundamentals and hence we do not see a breakout in prices,” said John Mothersole, IHS research director. “Chinese apparent consumption and imports still look strong compared to the continuing softness in Chinese industrial activity. This leads us to believe that much of the strength seen in Chinese data is in fact stock building, not actual physical use. This, coupled with a rise in U.S. interest rates, which we still assume to take place in September, should work to keep prices range bound over the near-term.”

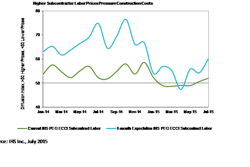

The current subcontractor labor index registered 49.0 in May, on par with the April reading, and still below the neutral mark. The majority of regions again registered flat labor costs in May, with Eastern and Western Canada as the only exceptions, posting a slight easing. For a fourth month running, the U.S. South reported flat labor costs. Nevertheless, tightness in skilled labor markets was still reported in the Gulf Coast.

The six month headline expectations index stabilized in May, rising to 50.3 after hitting a record low of 44.6 in April. This breaks a four month run since the beginning of 2015 in which the forward looking index consistently implied falling price expectations over the six month horizon. The materials/equipment index rebounded to 47.9 in May from 43.4 in April, but still indicated lower price expectations. That said, the underlying detail was fairly split with seven individual components registering higher price expectations, led by ready-mix concrete. Expectations for subcontractor labor rebounded to 55.8 in May after hitting a record low of 47.4 in April. Expectations rose across the board, driven by the U.S. South, with Western Canada as the only key exception.

To learn more about the new IHS PEG Engineering and Construction Cost Index or to obtain the latest published insight, please visit: www.ihs.com/ecci

![Fod No Caption 74 A Tc M Cy Uy[1]](https://img.forconstructionpros.com/mindful/acbm/workspaces/default/uploads/2026/08/fod-no-caption74atcmcyuy1.vcSFiPTy0m.png?auto=format%2Ccompress&fit=crop&h=100&q=70&w=100)

![Fod No Caption 74 A Tc M Cy Uy[1]](https://img.forconstructionpros.com/mindful/acbm/workspaces/default/uploads/2026/08/fod-no-caption74atcmcyuy1.vcSFiPTy0m.png?ar=16%3A9&auto=format%2Ccompress&dpr=2&fit=crop&h=135&q=70&w=240)