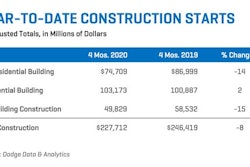

Single-family housing starts exemplify the construction economy’s COVID-19 heartbreak in the first quarter of 2020.

Total 2019 residential starts were 1.4 million units, just 0.3% above 2018, with single-family starts down 1,000 and multifamily up 1%.

[PODCAST] Update: How Much First Quarter GDP Report Dampens 2020 Construction Forecast

“We expected 2020 single-family starts to decline mildly again,” Richard Branch, chief economist with Dodge Data & Analytics told webinar attendees on April 9. “But Q1 was the best quarter since 2007 – 940,000 units (seasonally adjusted annualized rate).”

Then March became a tale of two months; housing starts growing early as the construction season unfolded, in line with March of 2019. And then the virus hit. Construction moratoria and stay-at-home orders in the last week doused so much work.

“Q2 home sales probably could fall by 50% compared to Q1, bringing us back to the levels we last saw during the Great Recession in 2007, 2008 and 2009,” Branch says. “And that could be optimistic, depending on how long the stay-at-home and physical-distancing requirements stay in place.

Details of Branch’s 2020 GDP forecast post-COVID-19

“The spring and probably the summer selling seasons are gone, and this weakness might continue into Q3.”

Dodge forecasts single-family starts to be down 10% in 2020, but begin to recover quickly with 5% growth in 2021.

Multifamily struggles harder

Multifamily construction didn’t start the year nearly as strong, with units falling in Q1 16% (-12% compared to Q1 2019). And its recovery prospects are not nearly as encouraging as single-family housing.

“This market has a lot more exposure,” Branch cautions. “We’re running 16 to 17 million in unemployment insurance claims. Jobs were down sharply in March. They will be down even more sharply in April. This will certainly lead to a pickup in delinquencies. This will put owners and developers into increasing financial difficulty.

“Vacancy rates ended 2019 at 4%; by the time we get to the end of 2020, they will be closer to 6%. In truth they would probably be much higher if it weren’t for local moratoriums on evictions. But even as the economy starts to recover, assuming that rent is just delayed and not forgiven, it will take time for renters to accumulate that back rent.”

Dodge forecasts multifamily starts to plunge 19% in 2020 and fall an additional 2% in 2021. “As we get into 2021, the multifamily market will also have to contend with growth on the single-family side,” Branch explains.

Warehouses undergird commercial building starts

“Given our assumptions of the track of the virus and macroeconomic assumptions, by the time we get to Q4 the level of (commercial building) starts activity is (expected to be) starting to return to the normal. With total 2020 commercial starts down 16%. But then forging ahead in 2021.”

Dodge forecasts the square footage of parking garage starts this year falling 29%, office starts dropping 13%, retail space down 33% and hotels and motels down 31%. Their biggest commercial building sector – warehouses – however, is only expected to slip 1%.

That’s particularly impressive when you consider warehouse construction set a Dodge Data record in 2019 with 336 million sq. ft. started.

Branch concedes that the portion of warehousing dealing with global trade will suffer from disrupted trade flow with the rest of the world, pushing up vacancy rates and suppressing starts. But the other big segment of warehousing is dedicate to ecommerce fulfillment, which of course has been flourishing during the coronavirus crisis.

Branch sees current conditions accelerating a more-permanent switch to on-line retailing. Pre-COVID-19, Amazon had telegraphed that it would continue building, but smaller (1 million sq. ft.) fulfillment centers instead of the 2 to 3 million sq. ft. centers of recent years.

“If you’ve tried to buy anything on Amazon in the last two or three weeks, you’ve noticed that the shipping times have been pushed out. I think there’s going to be a big push, particularly for Amazon, to carry larger inventories. I think Amazon will continue to push those 2- to 3-million sq. ft. distribution properties.

“Q1 was very strong in warehouse construction. Sharp decline in Q2. But this is a pure V (shaped progression). By Q3 and Q4 we’re right back up in this 330-million sq. ft. pace. So a record level in 2019, just a little bit off a record level in 2020, and you’ll notice a 7% increase there, breaking the record again, in 2021.”

Education supports institutional building

Total institutional building construction starts were initially forecast to decline 2%, and the pandemic pushed the Dodge Data forecast to -7%.

Education building is one of the largest nonresidential building sectors, running nearly as many square feet of starts as the office sector, and accounting for just under half of the total institutional construction. The COVID-19 effect is expected to cause education building starts to repeat its 2% 2019 decline in 2020. Dodge forecasts a 3% rebound in 2021, though, despite potentially significant financing challenges.

“Many states and local areas (governments) will suffer revenue shortfalls not just this fiscal year but next, at the same time the cost of social programs will be increasing,” Branch says. “So that could undermine the strength we’re seeing in the K-12 market and suppress construction activity.

“I think that going forward, colleges and universities will be placed under additional financial strain for a couple reasons: 1) there have been significant pushes by student bodies who are now at home to have room and board refunded. If that happens, that is money the universities have already committed, whether to overhead or to debt service. 2) Universities rely heavily on the returns from their endowment funds to fund capital improvement programs, and of course the stock market is still much lower than it was in February.”

Fast nonbuilding rebound?

Nonbuilding construction starts present a curious dynamic. The value of starts in the biggest sector – highways and bridges – was down 7% in 2019. The highway portion was flat and bridge construction was down sharply.

“First quarter data was particularly weak, so we’re starting from a much lower jump-off as we head into the forecast,” Branch says. “We’re expecting Q2 for highways and bridges to be down 12% from what we saw in Q1 – not as steep a drop as we saw in the building categories. Again a lot of infrastructure work has remained as an essential category, however we do need to keep in mind that workforce issues may delay some projects over the coming quarters.

“We do expect this category to have much more of a V-shaped recovery. Getting back in Q3 to where we were in Q1, and maybe closer to Q4 (2019). But the FAST Act does expire at the end of September, and of course that brings with it challenges as well as opportunities.

“We’re thinking that the plan that went through the senate public works committee unanimously will go through the house and the full senate and will have presidential approval probably within the next few months,” Branch suggests. “If that happens, the average level of spending within that replacement program is, on average, $10 billion a year higher than what we saw in the FAST Act. Certainly good news for 2021 in the highway and bridge sector. Potential for stimulus funding would certainly boost prospects into 2021 as well.”

Power and gas plant starts grew 124% in 2019 to $54 billion, which was expected to cut deeply into the sector starts in 2020. The Federal Energy Regulatory Commission has approved construction of a number of LNG facilities this year.

“But given where the global economy is and where natural gas prices are right now, we think that those projects get pushed out to ’21,” Branch predicts. “Which is why you have those numbers in ’21 pushed up 49% to $42 billion.

“This sector also contains utility grade solar and wind, and as those two sectors come much, much closer to grid parity they’re actually supporting some of the growth here and why we’re not seeing powerplant construction drop much further than $28 billion this year – it’s kind of a long-term historical normal level for power and gas.”