Nothing about 2020 fell within the realm of business as usual. It seems like there were surprises around every corner and the best prepared business plans were quickly laid to waste as contingency plans were hastily put in place to deal with one crisis after another. While the uncertainty of the 2020 election cycle is finally settled, and there are a couple of vaccines approved to combat the continuing COVID-19 pandemic, there is still plenty of uncertainty that makes it very difficult to forecast the future. The pandemic and its aftermath are expected to continue to plague the economy through at least the first half of the year. The vaccine will take time to produce and distribute.

In the meantime, construction backlogs and the construction material supply chain have been impacted. And despite the uncertainty, you still need to make a plan to address the upcoming year. To help you sort it all out, we contacted some of the construction industry’s most trusted sources about what they see for the months to come.

Q: What are likely to be the major drivers of the commercial and housing construction markets in 2021, and do you anticipate the current level of new construction to be sustained in both segments?

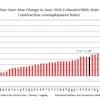

This year, we have seen a shift in housing demand preferences as a result of the COVID-19 pandemic, with home buyers and renters favoring lower density suburbs and exurbs over the core of large metropolitan areas. This suburban shift is seen in construction data, with the NAHB Home Building Geography Index (HBGI) showing that residential construction activity expanded at a more rapid pace in lower density markets. With this changing geography of housing demand, combined with record-low mortgage rates and a renewed focus on the importance of home, we expect demand will remain strong in 2021.

Supported by increased buyer interest, builder confidence remained near a data series high and sales have outpaced construction. Single-family construction is now at the highest level since the spring of 2007 and is expected to grow steadily over the next two years. However, builders continue to face challenges in terms of supply chain shortages of building materials and skilled labor as well as a lack of lots.

From a rental perspective, we expect multifamily construction to decline in 2020 and 2021 before stabilizing in 2022, although apartment construction will see strength in lower density markets.

Though home building and remodeling are relative bright spots for the overall economy, nonresidential construction will experience greater headwinds, as private nonresidential construction spending has seen a significant decline since January 2020.

Another trend is remote work, a pattern that gained momentum during the pandemic that could translate into less demand for traditional office space. But the work from home trend also supported a raging U.S. housing market in 2020 as people seek to acquire more space for dedicated home offices. This is also consistent with greater migration from cities to suburbs, which is already reflected in large-scale declines in apartment rents in some of America’s most expensive cities, such as San Francisco, New York City and San Jose. The multifamily market is less likely to generate as much construction activity as it did during the prior decade.

Richard Branch, chief economist, Dodge Data & Analytics (Dodge Data): The commercial construction space in 2021 will be somewhat of a mixed bag. On the upside, warehouse construction will continue to flourish as demand for e-commerce

Office construction should also begin its recovery in 2021, following a steep decline in 2020. While demand for new office space will be lower than years past, renovation activity will increase as landlords and developers push to improve their facilities by providing more physical space for workers and improved environmental attributes such as better air handling and washroom spaces.

Retail and hotel construction is expected to continue to languish in 2021, and indeed, won’t resume growth until there is widespread vaccine adoption. Since that is not expected until the mid-point of the year, it leaves little opportunity for growth in 2021.

Housing will be driven by strong demand for single-family construction in 2021. This is the result of the natural aging of the millennial generation as they grow their families, but also the pandemic-driven search for additional space away from dense urban areas. Increased flexibility resulting from remote working will aid this geographic shift. Multifamily construction will be weak in 2021 due to the supply overhang in large metropolitan areas.

Ken Simonson, chief economist, Associated General Contractors of America (AGC): There is huge pent-up demand for single-

Q: What are likely to be the major drivers for public construction in 2021, and do you anticipate the current level of new construction to be sustained? In which subsets do you expect to see the greatest uptick or downturn in activity?

ABC: Countervailing forces are at work in public construction. On one hand, weakened state and local government finances suggest weaker public works spending going forward. Despite the prevalence of low interest rates, many policymakers will probably seek to avoid putting more debt on public balance sheets.

On the other hand, given the battered state of the U.S. economy and the priorities of the incoming administration in Washington, D.C., federal spending on infrastructure could increase as part of a post-inauguration stimulus package. Republicans and Democrats do not agree on much, but leaders from both parties agree that America spends too little on infrastructure.

Public spending on infrastructure could rise over the next couple of years as the federal government steps up to assist our recovering economy, but that spending could fade quickly thereafter.

Dodge Data: The public sector — both building and infrastructure projects — will be reasonably stable in 2021. Given the growing gaps in state and local budgets across the country, this is somewhat positive news.

Street and bridge construction will see tepid growth in 2021 as federal funding provided through the one-year extension of the FAST Act is unchanged from the previous year. We fully anticipate that by the summer, a replacement for the FAST Act will be enacted providing for improved funding the following year. It is also likely that we will see a push from the Biden administration for an infrastructure package now that the Democrats have control of both the House and Senate.

On the building side of public construction, the largest project type is education. This sector was under great pressure in 2020 as the pandemic forced students out of their classrooms and into their homes. The fiscal issues facing state and local governments also weigh heavily on this sector’s ability to recover, meaning 2021 is likely to be another down year for education construction.

AGC: Any growth in public construction will depend on early passage of federal funding for infrastructure and relief for state and local governments. Unless this occurs early in the year, the impact on projects is unlikely to be felt until 2022 or later.

Highways have the greatest chance of receiving additional funding. But there will also be a push to fund transit and other passenger rail projects; alternative energy production, storage, and charging facilities; and possibly public hospitals and care facilities.

The weakest public markets are likely to be public universities and colleges and other types of public buildings such as office and judicial system buildings.

Q: What factors could play an instrumental role in raw material costs in 2021? Will the ongoing COVID-19 pandemic have any impact on the costs of raw materials or other construction inputs?

NAHB: The issues that have limited housing supply in recent years, including land and material availability and a persistent skilled labor shortage, continue to place upward pressure on construction costs.

The result of insufficient supply to meet soaring demand has caused prices of building materials, most notably lumber, to skyrocket this year. Between mid-April and mid-September, lumber prices soared more than 170% due to reduced domestic production during the pandemic. NAHB data showed spikes in softwood lumber prices earlier in 2020 caused the price of an average new single-family home to increase by $16,148. While prices fell from September to November, lumber costs are rising once again as production remains limited and housing demand is strong headed into 2021.

As tariffs contributed unprecedented price volatility leading to higher prices and harming housing affordability, the U.S. Commerce Department has recently made the decision to reduce its duties on shipments of Canadian lumber into the U.S., down to roughly 9% from more than 20%. The tariff reductions were expected to go into effect in mid-December. Lower tariffs would mitigate uncertainty and associated volatility that has plagued the marketplace, which could help ease upward pressure on lumber prices.

Beyond lumber, there are other material costs that are elevated. Additionally, appliances and materials are taking longer to deliver, extending construction times and increasing costs.

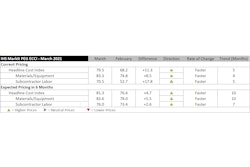

ABC: For the most part, construction materials prices have behaved, with exceptions like softwood lumber. Production capacity of this lumber has been constrained recently for several reasons. When home builders began placing large softwood lumber package orders, suppliers were not prepared for the rush and prices took off.

Once vaccines become broad-based globally... similar dynamics may become apparent for commodities such as steel, oil and copper as the global economy comes racing back after a period of slumber. That could set the stage for large-scale increases in construction input prices at some point in 2021. That is an important point to consider as people enter longer-term commitments presently.

Dodge Data: One of the key factors will be the new administration’s views on tariffs on construction-related goods from China, Canada and elsewhere. Additionally, increased levels of construction activity in 2021 will put upward pressure on materials prices and wages.

AGC: Materials costs are likely to remain volatile as the U.S. and global economies expand or pause. Bottlenecks and supply chain disruptions may crop up again, depending on the severity of COVID-19 outbreaks.

Q: How has the COVID-19 pandemic impacted the continued labor shortage plaguing the construction industry? What are your projections for the labor market in 2021, particularly when it comes to skilled trades?

The U.S. Bureau of Labor Statistics November data shows that over the past seven months, job gains in residential construction offset 96% of the jobs lost in March and April, while there has only been a 58% job recovery in nonresidential construction. However, in any given month, there is still a shortage of 200,000 to 300,000 workers. Looking forward, the job openings rate is likely to experience choppiness in the months ahead given divergent outlooks within the construction industry.

As the construction skilled labor shortage remains a key challenge for residential and nonresidential construction firms, training and adding new workers is an important goal of the industry as we have seen an aging workforce in the skilled trades. A labor shortage will lead to higher housing costs and increased home prices, and make housing less affordable for buyers.

To help close the gap on the labor shortage, the housing industry needs to continue to invest in training to attract younger workers who may not have considered a career in construction or have been inordinately affected by the pandemic and recession. Workers trained in the building trade skills will increase productivity and further lower construction costs to consumers.

Bringing additional women into the construction labor force also represents a potential opportunity for the future. A recent NAHB study found that the number of women employed in the construction industry grew substantially in 2019, surpassing the peak pre-recession employment level.

ABC: Despite the loss of nearly 200,000 construction jobs over the course of the pandemic, shortages of skilled construction workers will persist. Many of America’s most skilled construction workers are approaching retirement age, and the next generation has still not entered the skilled trades in sufficient numbers.

History indicates that when construction workers lose jobs, they often leave the industry altogether. All of this suggests that while it may be marginally easier to recruit talent now than prior to COVID-19, structural issues remain.

Dodge Data: The construction sector will continue to be plagued by the lack of skilled and available labor in 2021. While the number of job openings in construction has fallen since the pandemic began, there are still, on average, more open positions in the industry currently than there were in 2017. The demand for workers is down, but not out, and will certainly rebound sharply in 2021 as construction picks up.

AGC: Many contractors report projects are taking longer to complete, either because fewer workers are allowed on site at one time, workers are kept home by illness (their own, a family member’s or the need to provide dependent care), or delays and shortages of materials. While the decline in nonresidential projects will mean fewer companies are hiring and more workers are laid off, contractors that are trying to hire are still likely to have difficulty finding willing applicants with the right skills.